-

Going Global: A Founder’s Playbook

1) Why go global? Triggers for expansion

The timing of international expansion is as important as the destination. Research suggests around 55% of successful scale-ups expand abroad within their first five years, with B2B SaaS companies often moving earlier to capture global network effects.

Typical triggers include:

- Saturation of the local market: Growth at home begins to plateau or CAC rises because the easiest wins are taken. Many UK fintechs (Monzo, Starling) looked to the EU once domestic growth slowed.

- Low-hanging fruit abroad: Certain regions have less competition but high demand. US SaaS start-ups often expand into Europe for volume, while European start-ups go to the US for higher ARPU.

- Following customers: Roughly 40% of SaaS expansions are client-led—a major customer requests coverage in another geography. Stripe expanded this way, localising payment rails to meet developer demand.

- Talent pools: Some regions provide scarce capabilities, such as AI research in Toronto, engineering in Eastern Europe, or design in Berlin.

- Capital and incentives: Government support often tips the balance. Singapore offers tax holidays for tech investors, Ireland has the 12.5% trading tax rate, and Innovate UK regularly funds pilots.

- Strategic positioning: Securing approvals, pre-empting competitors, or building brand visibility in a key region. Revolut pursued EU licences early to maintain access post-Brexit.

The right moment is when domestic operations are stable—with repeatable sales motion, predictable unit economics, and leadership capacity to focus abroad without weakening the home base.

2) Choose an entity model that won’t paint you into a corner

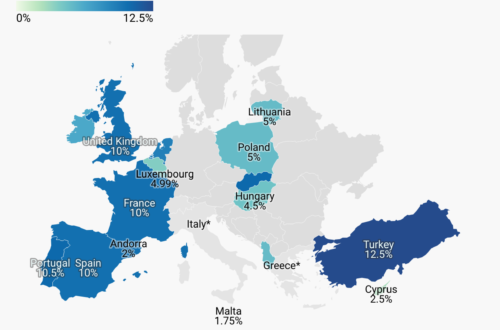

Parent HoldCo (e.g., UK Ltd or Delaware C-Corp) provides a clean cap table for investors, central place for IP and equity plans.

Regional Subsidiaries are used for hiring, sales contracts, and tax compliance:

- Ireland (IE) for EMEA: 12.5% tax; EU access

- UK for EMEA/Global: 25% main tax; strong investor familiarity

- Singapore for APAC: 17% tax; incentives; locally resident director required

- UAE (Free Zones) for GCC: 9% federal CIT; 0% in some zones; good for project-based presence

IP location: Keep IP at Parent for investor clarity and licensing flexibility.

3) Trading, tax, and compliance—avoid the hidden tripwires

- Permanent Establishment risk if staff or contracts are local.

- Indirect taxes: VAT/GST obligations for digital services.

- Transfer pricing: Intercompany agreements required.

- Employment: Follow local law on payroll, benefits, and contractor conversion.

- Data and privacy: GDPR and cross-border rules.

- Licensing: Fintech, health, and energy often need permits.

- Commercial terms: Local payment cycles, governing law, and SLAs.

4) Operating model without chaos

- Core/Hub/Spoke model: Parent retains IP, brand, finance; hubs run regional sales/support; spokes via partners.

- Finance: Multi-entity accounting and FX strategy.

- People: Unified global structure with local addenda.

- Security: One ISMS (e.g., ISO 27001) with local data hosting as needed.

- Go-to-market: Localised pricing, sales collateral, and references.

5) Phased entry that works

- Beachhead: Sell via Parent; 1–2 hires through PEO/EoR.

- Entity setup: Incorporate, register tax/VAT, payroll.

- Scale: Hire, build partnerships, expand marketing.

- Optimise: Refine TP, incentives, evaluate new hubs.

6) Market size signals

- Global SaaS market projected at $908bn by 2030.

- 55% of high-growth start-ups expand abroad within five years.

- Client pull is a top trigger, especially in SaaS and clean tech.

7) Real expansion examples

- Revolut: Built regulatory strength with EU licences.

- Uber: Blitz-scaled but retreated in China—regulation and local dynamics matter.

- Airbnb: Adapted trust/safety and policies for local acceptance.

- Stripe/Shopify: Expanded by simplifying local compliance for customers.

8) Global Entity Comparison for Start-Ups

Region / Country Typical Use Case Corporate Tax Rate Entity Setup Time Payroll / Employment Incentives & Notes UK Parent HoldCo or EMEA hub; investor familiarity 25% main rate (19% for small profits, marginal relief in between) 2–3 weeks Strong employee protections; auto-enrolment pensions R&D tax credits, Innovate UK grants, SEIS/EIS for investors Ireland EMEA hub; tech & SaaS clustering 12.5% trading rate (15% for €750m+ groups) 2–3 weeks Flexible employment law; local payroll setup needed Grants from Enterprise Ireland; strong EU base Singapore APAC hub; gateway to SE-Asia 17% (incentives can reduce to ~0–10%) 1–2 weeks At least one locally resident director; CPF contributions Pioneer incentives, strong IP protection, ASEAN access UAE (Free Zones) GCC hub; project-driven presence 9% federal CIT (15% for €750m+ MNEs) 2–6 weeks No income tax; visas required 0% on qualifying free zone income, strong infra for energy, logistics 9) Recommendation flow (If/Then)

- If raising VC in Europe → Base Parent in UK or Ireland; Ireland for tax efficiency, UK for investor familiarity.

- If targeting APAC growth → Singapore is the default hub.

- If bidding for GCC projects → UAE Free Zone entity offers speed and credibility.

- If global investor signalling is key → UK Ltd or Delaware C-Corp parent, with subs layered in regionally.

10) Founder checklist

- Market pick: 1 flagship per region.

- Entity & tax: Subsidiary setup, VAT/GST, TP policy.

- People: Local employment law compliance.

- Data & security: Hosting strategy, DPAs.

- Banking: Multi-currency and FX planning.

- Commercials: Localised MSAs and SLAs.

- Governance: Regional scorecards for ARR, CAC, margins.

Bottom line

Global expansion is a trigger-driven process—whether from saturation at home, low-hanging fruit abroad, or customer pull. With the right sequencing, entity setup, and compliance foundations, start-ups can make internationalisation a growth multiplier rather than a distraction. Choosing the right hub—UK, Ireland, Singapore, or UAE—depends on strategy, stage, and investor lens.

-

Pitch Decks and Information Memorandums

Securing investment is one of the defining challenges for a founder. Capital fuels product development, hiring, scaling operations, and entering new markets. But before a cheque is signed, before a due diligence call is scheduled, there’s usually one hurdle that decides whether you even get a seat at the table: the pitch deck.

For many founders, the deck is both an opportunity and a trap. Done well, it translates vision into something investors can believe in. Done poorly, it undermines credibility and shuts doors before they’ve even opened.

The truth? Investors are inundated with decks. A typical VC reviews hundreds every month. Only a fraction make it through to partner discussions, and fewer still convert into funding. Understanding what makes a deck succeed, and how it differs from the longer-form Information Memorandum, is critical.

The Anatomy of a Great Pitch Deck

The best decks are clear, concise, and compelling. They strip out noise and present a story investors can immediately grasp. Most strong decks follow a similar structure:

- Problem – What pain point exists in the world? Why is it urgent or costly?

- Solution – How your product or service addresses that pain better than alternatives.

- Market – Size of the opportunity (TAM, SAM, SOM). Why now?

- Traction – Evidence it’s working: paying customers, growth metrics, partnerships.

- Business Model – How you make money, and why it’s scalable.

- Go-to-Market – The plan for acquiring and retaining customers.

- Competition – Who else is tackling this problem, and why you have the edge.

- Team – Why you’re the right people to deliver this.

- Financials – Ambitious but credible projections, assumptions, and unit economics.

- The Ask – How much you’re raising, what it’s for, and what investors get in return.

Rule of thumb: keep it to 10–15 slides. Each slide should make one clear point.

What the Data Shows About Investor Behaviour

Investors don’t read decks like novels, they skim, scan, and zoom in on what matters most.

- 3 minutes 44 seconds: Average time spent reviewing a deck (DocSend 2022).

- Traction slide: Most heavily scrutinised, with 23% more time spent than average.

- Financials and Team: Close behind; investors need proof the numbers add up and the people can deliver.

- Problem and Solution: If these aren’t crystal clear, drop-off is immediate.

- Success rate: Only 1% of decks lead to funding (HBR, 2021).

The deck’s job isn’t to answer every question — it’s to earn you a meeting.

Real Examples of Successful Decks

Airbnb (2009): A 10-slide deck that clearly explained the problem (expensive hotels, lack of authenticity), the solution (renting from locals), and the market. Raised $600k seed.

Uber (2008): Highlighted inefficiencies in black car services, with a realistic TAM. Raised $200k seed.

Buffer (2011): Publicly shared simple deck, with traction metrics front and centre. Raised $500k seed.

Front (2016): Balanced traction with team credibility, raising $10m Series A.The common thread? Clarity and evidence beat complexity every time.

Common Mistakes That Kill Investor Interest

Even great ideas can be undermined by bad decks. The most frequent mistakes include:

- Overloading with detail – A deck is not a business plan.

- Unclear problem – If investors don’t get the pain point, they won’t buy the solution.

- Fantasy projections – Hockey-stick growth without rationale destroys credibility.

- Ignoring competition – Claiming “no competitors” signals naivety.

- Weak team slide – Investors want to know who’s steering the bus.

- Forgetting the ask – Too many founders never state how much they’re raising.

- Poor design – Sloppy visuals imply sloppy business.

Pitch Deck vs. Information Memorandum

Founders often confuse a pitch deck with an Information Memorandum — but they serve different purposes.

Pitch Deck – The Door Opener

- Purpose: Spark interest, secure a meeting.

- Format: 10–15 slides, visual and concise.

- Tone: Narrative, high-level, designed to intrigue.

- Investor Time: Minutes.

Think of it as the movie trailer.

Information Memorandum – The Due Diligence Starter

- Purpose: Provide detail for serious evaluation.

- Format: 20–40+ page document.

- Content: In-depth business model, market analysis, governance, risks, detailed financials.

- Tone: Analytical, evidence-heavy.

- Investor Time: Hours.

This is the reference manual.

The distinction matters. Sending an IM too early overwhelms investors. Sending only a deck frustrates those who are serious. The deck gets you the meeting; the IM supports the deal. Together, they form a natural progression:

Pitch Deck → Meeting → IM → Data Room → Term Sheet.

Tips for Founders

- Think investor-first – Shape every slide around what they need to believe.

- Tell a story – Take investors on a journey from problem to opportunity.

- Show traction early – Even small wins prove demand.

- Use numbers strategically – A few credible datapoints beat endless adjectives.

- Rehearse delivery – A deck is only as strong as the way you present it.

Final Thought

A pitch deck won’t guarantee you funding, but a weak one will almost guarantee you won’t get it. The perfect deck is not about flashiness or 50-slide deep dives. It’s about clarity, credibility, and sparking curiosity.

Then, once investors are leaning in, the Information Memorandum and data room give them the detail to commit.

As the saying goes: the deck gets you the meeting, not the money.

-

Cyber-attacks and why SMEs are particularly vulnerable

What Recent Attacks Have Looked Like

In 2025, several high-profile cyberattacks have dominated headlines in the UK, showing both old and evolving threats:

- Jaguar Land Rover (JLR) was hit by a major cyberattack in September 2025, forcing production shutdowns in the UK and disrupting its global supply chain, costing the business hundreds of millions per week.

- Marks & Spencer was targeted earlier in 2025, with ransomware disrupting Click & Collect and contactless payments, knocking out automated stock systems, and leading to estimated operating losses of £300 million.

- Synnovis, an NHS lab services provider, suffered a ransomware attack in mid-2024, costing an estimated £32.7 million, crippling diagnostic services across London hospitals.

These incidents involved ransomware, phishing, and supply chain vulnerabilities — proving that even well-resourced firms are exposed.

Origins & Motivations

Most recent UK attacks trace back to organised criminal groups such as Scattered Spider, Lapsus$ and DragonForce, often based in Eastern Europe or Asia.

Motivations include:

- Financial gain: ransom payments, stolen data resale, blackmail.

- Operational disruption: halting production or services to force negotiations.

- Reputational leverage: damaging brand trust to pressure settlements.

Methods vary, but many breaches start with phishing, vishing, weak authentication, or unpatched systems.

How Vulnerable SMEs Are

SMEs are particularly at risk because:

- Limited budgets often mean no full-time security staff.

- Fewer preventive controls such as multi-factor authentication, network segmentation, and backup strategies.

- A single breach can threaten business continuity, cashflow, and survival.

- Many SMEs sit within larger supply chains, making them indirect targets.

Market data is sobering: cyber attacks have cost UK businesses an estimated £44 billion over the past five years. SMEs face average direct costs of £3,400–£5,000 per incident, not including reputational damage and lost contracts.

The Importance of Cyber Insurance

Cyber insurance has become a critical safeguard:

- Covers direct financial losses from ransomware, downtime, and business interruption.

- Supports recovery with access to specialist incident response teams, legal counsel, and communications advisors.

- Mitigates liability in the event customer or employee data is compromised.

- Protects balance sheets when attacks escalate beyond what an SME could absorb alone.

Yet many SMEs remain uninsured or underinsured, often on the advice of IT providers who downplay the risk. The reality is that cyber insurance is now viewed by boards and auditors as part of a standard risk management framework, alongside firewalls and backups.

How Investors View Cyber Risk

Investors increasingly assess cyber security posture as part of due diligence:

- Private equity and venture capital investors know that a portfolio company breach can wipe out value. They look for strong governance, security certifications, and cyber insurance as indicators of maturity.

- Institutional investors are asking ESG-linked questions about cyber resilience, data governance, and operational risk exposure.

- Banks and lenders now factor cyber risk into credit decisions — businesses without basic protections may face higher borrowing costs or limited access to debt.

A PwC report in 2024 found that over 70% of institutional investors consider cyber security a “make-or-break” factor when investing in digital-first businesses. Companies without insurance or demonstrable resilience are increasingly penalised in valuation discussions.

Taking Guidance & Sensible Precautions

To protect against these risks, SMEs should:

- Carry out regular risk assessments and penetration testing.

- Train employees on phishing and social engineering threats.

- Enforce multi-factor authentication and regular patching.

- Develop a clear incident response plan.

- Ensure regular, secure backups of critical systems.

- Take out appropriate cyber insurance to limit financial exposure.

Conclusion

Cyberattacks are no longer abstract — they are shutting down factories, blocking supermarket shelves, and straining healthcare systems. SMEs are especially vulnerable, both as direct targets and as weak links in larger supply chains.

The cost of underestimating the threat is measured in billions, while the cost of preparation is modest by comparison. For SMEs looking to survive, scale, and attract investment, cyber resilience and insurance coverage are no longer optional — they are essential.

-

The Future of Sustainable Energy Source Technologies

1. Global Momentum in Clean Power and Storage

The global energy transition has entered a decisive phase,

~700 GW of renewable capacity was added in 2024, the 22nd consecutive record year, Renewables generated 32% of global electricity last year

Battery storage is surging, with ~97 GWh installed in 2024 alone, and 2025 projected to set another record

Costs are falling fast: Lithium-ion battery pack prices averaged $115/kWh in 2024, a 20% year-on-year drop

Capital is flowing: More than $2 trillion was invested in clean energy in 2024, outpacing fossil fuel investments globallyThis combination of accelerating deployment, lower costs, and surging investment is reshaping not only power generation and industry but also culture, hospitality, and live events.

2. The Rise of Battery Technology

What’s Bankable Today

Lithium-ion (LFP/NMC) dominates grid-scale and commercial applications, typically for 1–4 hour storage,

Solar + Storage is now mainstream, helping businesses and communities avoid peak energy charges and reduce grid dependence,

Corporate demand for sustainability (hyperscalers, EV fleet operators, hospitality) is pushing banks and funds to see storage as a core infrastructure asset,What’s Emerging

Sodium-ion: Lower cost and safer chemistry, CATL’s new “Naxtra” cell offers 175 Wh/kg energy density, with mass supply expected 2025–2026

Long-Duration Energy Storage (LDES):

Iron-air (Form Energy): Demonstrations underway with 100-hour discharge potential

Flow batteries: Iron and vanadium flow technologies are scaling manufacturing and securing pilot deploymentsThese new chemistries will complement lithium-ion, making 24/7 clean power achievable and supporting resilience in energy-intensive sectors.

3. Investor Appetite Across the Capital Stack

Seed/Pre-seed: Materials innovation, AI-driven energy management, and novel chemistries, Investors seek strong IP and pilot-ready concepts,

VC (Series A/B): Companies with early revenues and repeatable deployment models, Key ask: proof of reliability and customer adoption,

Growth Equity: Focus on manufacturing scale-up, supply chain integration, and backlog of contracts,

Infrastructure & Project Finance: Large-scale, de-risked storage projects, often in the 50–500 MW class, attracting billions in debt and equity,Dedicated storage financings reached $17.6 billion across 83 deals in the first three quarters of 2024, underlining institutional appetite

4. Transformation in the Events Industry

The live events sector is undergoing a sustainability revolution, Traditionally reliant on diesel generators, festivals and stadium tours are now testbeds for cutting-edge clean energy solutions,

Coldplay, Showpower, and Hope Solutions — a Case in Point

For their recent world tour, Coldplay pledged to cut direct emissions by 50% compared to their 2016–17 tour, Delivering on that ambition required an innovative energy strategy,

They partnered with Hope Solutions, a sustainability consultancy specialising in live events, to design and manage the shift to renewable power and lower-carbon logistics.

The tour incorporated mobile battery systems provided by companies like Showpower, replacing polluting diesel generators, These containerised lithium-ion units were integrated with renewables and onsite charging infrastructure, providing reliable, quiet, and emission-free power,

Audience participation became part of the energy story: kinetic dance floors and static bikes allowed fans to generate electricity during shows,

The wider approach included sustainable aviation fuels, reforestation, and investment in carbon capture technologiesto address residual emissions,The result: a tangible demonstration that large-scale tours can dramatically reduce carbon impact without compromising on performance or audience experience, Coldplay and their partners turned sustainability from a backstage detail into a headline feature, showing what the future of live entertainment looks like,

Why It Matters

The global live events market is valued at $652 billion (2023) and forecast to reach $1.2 trillion by 2032, Sustainability will be a major determinant of growth and reputation,

Large festivals can consume over 250,000 litres of diesel in a weekend, emitting ~2.68 kg CO₂ per litre burned — a reputational risk and a cost issue,

Battery-powered solutions can cut on-site event emissions by 50–70%, while offering cost savings on fuel and logistics,5. What the Future Holds

Sustainable events will become mainstream, Within the next decade, battery-powered stages and festival sites will be the norm, Diesel generators will be viewed as outdated,

Cross-sector convergence, The same containerised battery systems serving concerts will also support hospitality, lodge parks, sports facilities, and EV charging hubs,

Financing innovation, Blended models will emerge: infrastructure-backed “power-as-a-service” offerings for festivals, alongside VC/growth equity to fund new technologies like sodium-ion,

Global expansion, New festival and sports markets in the Gulf, Africa, and Latin America could leapfrog directly to sustainable infrastructure,6. Takeaway for Investors

Sustainable energy technologies are no longer just a grid play, they are reshaping how people live, travel, and experience culture, The Coldplay + Hope Solutions + Showpower case demonstrates that batteries can transform industries well beyond utilities, creating new revenue models and cultural relevance,

For investors, the opportunity lies in,

Backing emerging chemistries (sodium-ion, LDES) at seed and VC stage,

Funding platform scale-ups that package batteries into event-ready, park-ready, or EV-ready solutions,

Deploying capital at infrastructure scale into proven solar-plus-storage and standalone BESS projects,The energy transition is here, and the industries adopting it fastest, from music to hospitality, will set the tone for investors and audiences alike,

-

Sustainability behind the scenes at Coldplay’s Music of the Spheres World Tour

I was first introduced to Showpower by Lukas Howell of Hope Solutions over a year ago and picked things up with them again earlier this year. Since then, we’ve been working closely with Rob and Tim to help scale a business that has the potential to transform how live events are powered.

This week, Georgina Chapman and I caught up with Rob Scully and Tim Benson at Wembley, just ahead of Coldplay’s final UK concert. Next week, the Kognise team will be joined by Richard Lydon as we head over to Amsterdam with the Showpower team to continue shaping the next stage of their journey.

The Coldplay Blueprint

When Paul Schurink, Rob Scully and Tim Benson, then at ZAP Concepts, were approached by Lukas Howell and Coldplay’s Sustainability Manager, the challenge was clear: create the most sustainable, flexible, and reliable power system possible for a global stadium tour.

The result was Showpower: a state-of-the-art, mobile, modular power system that can run 100% of any stadium show, anywhere in the world, powered by renewable energy and batteries instead of diesel.

This was put to the test on Coldplay’s Music of the Spheres World Tour — the most attended and highest grossing tour in history, projected to reach 13 million tickets and $1.4bn in revenue by September 2025.

And crucially, it has been the most sustainable stadium tour ever delivered:

- 59% reduction in CO₂ emissions compared to their 2016-17 tour.

- Nearly 7 million trees planted, one for each ticket sold.

- 72% of tour waste diverted from landfill.

- Renewable energy integrated from solar, kinetic dance floors, power bikes, and SmartGrid battery systems.

Hope Solutions and Showpower

Hope Solutions, under Luke Howell, shaped the sustainability framework and independently validated results with MIT’s Environmental Solutions Initiative. Showpower, through its SmartGrid and Power-As-A-Service model, provided the technology backbone, demonstrating that large-scale events can now be powered without diesel, reliably and at scale.

Looking Ahead

What has been proven with Coldplay is just the beginning. Showpower’s technology, this is about building a strategy, plans and the funding to accelerate growth, scale globally, and set a new standard for powering live events sustainably.

-

Coaching Boards: Unlocking the Full Potential of Your Business

In every business, whether it is a start-up fighting for survival, an SME pushing hard for growth, or a larger organisation navigating complex challenges, the boardroom sets the tone for everything that follows. The decisions made at the board table do not just stay in the boardroom. They ripple out across the business, shaping the way teams work, the way clients are treated, and ultimately how successful the business becomes.

Despite this enormous influence, boards are rarely given the same support and development opportunities as executives or leadership teams. We often see investment in coaching for CEOs, senior managers, or department heads. Yet the very group responsible for oversight, governance, and long-term strategy is too often left to work things out for themselves.

This is a missed opportunity. A board that is coached to perform well together becomes a more aligned, more resilient, and ultimately more effective leadership group. And when the board is strong, the entire business benefits.

Why Coaching a Board Matters

Coaching a board is not about suggesting that something is broken. It is about recognising that the collective performance of a board can be multiplied when members are supported to operate at their best. There are several clear benefits to putting time and resource into board coaching.

First, coaching creates alignment of vision and values. Even the most talented directors will bring different perspectives to the table. Left unchecked, those perspectives can pull the business in conflicting directions. Coaching allows the board to step back, clarify the company’s vision and values, and agree on a common purpose. This alignment means everyone is moving in the same direction and decisions are made with consistency and clarity.

Second, it improves decision-making. Diversity of thought is a huge strength for any board, but it can also lead to friction or even stalemate. Coaching ensures that diverse opinions are channelled into constructive debate. It helps members challenge one another in the right way and creates the conditions for smarter, more balanced decisions.

Third, coaching builds trust and resilience. High performing boards are built on trust. Coaching creates a safe environment where difficult conversations can be had without personal conflict. Over time this builds resilience. Boards that trust one another are far more capable of dealing with crises or sudden shifts in the market.

Fourth, coaching prepares boards for investors and external scrutiny. Investors are not just interested in the numbers on a spreadsheet. They are assessing whether the board itself has the capability and credibility to deliver. A coached, professional, and cohesive board inspires confidence. It is often the deciding factor in whether investment is made.

Finally, coaching helps boards adapt to scale. What works in a start-up will not work for an SME, and what works in an SME will not be sufficient for a larger business with multiple stakeholders. Coaching supports this evolution. It helps boards transition from entrepreneurial energy to structured governance and from reactive decision-making to long-term strategic planning.

How Coaching Can Be Delivered

There is no one-size-fits-all approach to board coaching. Different boards will need different types of support depending on their stage of growth, their composition, and their challenges.

Board workshops are often the starting point. These structured sessions bring the entire board together to work through issues such as roles, governance frameworks, or long-term strategy. They are especially powerful when the business is preparing for change, such as a funding round or a transformation project.

Individual coaching for board members can also be extremely effective. Many founders in particular benefit from this, as they move from being entrepreneurial leaders into governance roles. Individual coaching provides space for reflection and personal development that board meetings alone cannot provide.

Peer review and 360-degree feedback are another option. Gathering structured feedback from other board members and from senior staff in the organisation gives directors a clear view of their strengths and blind spots. This information is invaluable in shaping their contributions at board level.

Scenario-based coaching takes the board through simulated challenges. For example, they might be coached through how they would handle a sudden cashflow crisis, a major investor negotiation, or the arrival of a new competitor. This type of coaching strengthens their ability to work together under pressure and exposes any gaps in preparation.

Finally, ongoing advisory support can be transformational. This involves having a fractional coach or advisor embedded with the board, attending meetings, and providing real-time feedback. This continuous involvement ensures accountability and helps the board embed new behaviours over time.

The Payoff for Businesses and Investors

When boards are coached, the results are visible across the business. Decisions are made faster and with greater confidence. Investors see a professional and credible leadership team that takes governance seriously. The organisation gains clarity on strategy, culture, and direction. Internal conflicts are reduced and replaced by constructive challenge. And perhaps most importantly, a coached board sends a signal to the rest of the business that leadership is disciplined, united, and prepared for the future.

For investors, this matters enormously. In many cases, the people side of the business is as important, if not more important, than the financials when deciding whether to back a company. A strong, coached board gives investors confidence that their capital will be well stewarded. For founders, it is the difference between a board that simply shows up to meetings and one that drives real, transformative progress.

Final Thought

Every business, no matter its size, can only grow as far as its leadership allows. Boards set the direction, model the culture, and hold the responsibility for long-term success. Coaching a board is not a luxury. It is a multiplier. It transforms a group of individuals into a high-performing leadership team capable of carrying the business through challenges and towards opportunity.

The right coaching, delivered at the right time, can unlock potential that even the board members themselves did not realise was there. For businesses serious about growth and for investors serious about returns, coaching the board may well be one of the smartest investments you can make.

-

Why a Balanced Board Makes or Breaks a Business

I’ve spent enough time inside boardrooms, from start-ups through to mid-sized companies and bigger organisations, to know that one thing always makes the difference: the board.

You can have an exceptional product, a strong order book, or even a decent chunk of capital in the bank. But if the board isn’t balanced, doesn’t cover the right skills, or isn’t capable of challenging itself constructively, the business will stumble. In too many cases, it fails completely.

And investors know it. In fact, when they’re assessing a business for funding, they often spend as much time scrutinising the people as they do the numbers. A weak board is one of the biggest red flags. A strong, balanced board is one of the greatest value signals.

What a Balanced Board Really Means

A board isn’t just a group of people with titles. It’s a mechanism for protecting and driving the business. That requires balance.

At minimum, a board should cover these areas:

Finance: Discipline in forecasting, visibility on margins, cashflow management, and risk oversight. Too many boards rely on lagging information rather than forward-looking control.

Sales and Marketing: Growth doesn’t happen by accident. Boards need members who understand customer acquisition, brand building, market entry, and pricing strategies.

Operations and Delivery: A business that can’t deliver profitably is finished before it scales. Boards need people who can stress-test delivery assumptions and ensure operational scalability.

Strategy and Growth: Vision is non-negotiable. Someone must be looking at the bigger picture: spotting trends, evaluating adjacencies, and ensuring the company doesn’t get locked into short-term firefighting.

Governance and Compliance: It’s not glamorous, but investors need confidence that the business is properly governed, protected, and aligned with regulatory expectations.

People and Culture: Often ignored, but central. If the board doesn’t understand culture, retention, and leadership, the whole thing will crack eventually.

No one individual can cover all of these. But collectively, they must be there. If even one or two are missing, the board is unbalanced and the business exposed.

Where Boards Go Wrong

The most common mistake is keeping people in roles out of loyalty. Founders often place early employees, supportive friends, or long-standing investors onto the board. They might have been valuable in the early stages, but once the business moves forward, the demands change.

I’ve seen scale-ups heading into £10M plus revenue with boards that look like they belong to a start-up. I’ve seen SMEs holding onto directors who’ve added no value in years, purely because “they were there from the start.” I’ve seen larger organisations where board members attend, nod, and leave, offering nothing beyond presence.

The hard truth is this: a business that grows needs a board that evolves. If the skills don’t match the stage, it’s a liability.

Switching people out isn’t disrespectful. It’s an acknowledgement that the company comes first. Their contribution can be recognised without compromising the future.

Why Investors Care So Much

Investors rarely believe a forecast. They know plans shift, markets change, and the numbers are often optimistic. What they do believe in is people.

When they assess a board, they ask:

Does this team know how to deliver growth at this scale?

Are they credible with future funders, customers, and partners?

Will they challenge each other, or just nod along?

Are they open to change and coaching?

Is the governance framework protecting the company’s value?That’s why you often see investors attach conditions to funding. It’s not unusual for a term sheet to include a requirement for a CFO, an independent non-executive director, or even the replacement of a founder-CEO who isn’t fit for the next stage.

And they’re not wrong. Research consistently shows that businesses with experienced, balanced boards raise more capital, grow faster, and survive longer.

The Investor Lens

The saying is simple but true: investors would rather back an “A team with a B product” than the reverse.

Why? Because the right team will adapt. They’ll pivot when needed, restructure when required, and find a way through challenges. The wrong team will cling to their comfort zone and burn even the best opportunity.

I’ve seen investors walk away from companies with strong traction purely because the board was dysfunctional or lacked credibility. I’ve also seen investors pour millions into businesses with flawed products but exceptional teams, and watch those teams pivot into new markets successfully.

A balanced board signals discipline, maturity, and resilience. An unbalanced one screams risk, blind spots, and fragility.

The Role of Competencies

It’s easy to think of a board as a collection of personalities. But investors see it as a collection of competencies.

When I’m assessing a board, I ask myself:

• Who’s covering finance and can they hold a model up to the light?

• Who’s challenging sales assumptions and pushing for real market evidence?

• Who’s ensuring delivery can actually meet what’s being promised?

• Who’s looking three to five years ahead and checking we’re not just building short-term fixes?

• Who’s making sure culture and people aren’t left behind?If I can’t see names against those boxes, I know the business has gaps. And so will investors.

Why This is Hard for Founders

Founders often struggle with this because it feels personal. The business is their creation, and the early team are often friends or loyal colleagues. But as one investor told me bluntly: “We’re not investing in who got you here. We’re investing in who can take you there.”

The most successful founders are the ones who can step back and let their boards evolve. They accept that their role changes over time. They let professionals with the right skills take the wheel where needed.

The least successful are the ones who cling on. They resist governance, reject oversight, and treat board seats as rewards. Almost always, those businesses stall or collapse

Final Thought

Every business, no matter the size, is powered by people. And at the top, the board sets the tone, direction, and resilience for everything that follows.

If you’re a founder, the uncomfortable question you need to ask is this: does your board really have the balance and competence to take the business forward? Or is loyalty, ego, or inertia stopping you from making the changes you need?

If you’re an investor, you’re already asking this. And your decision to invest will depend heavily on the answer.

The businesses that face this honestly, that balance their boards, add the missing skills, and make tough calls, are the ones that scale, attract capital, and build long-term value. Those that don’t, almost always get stuck, distracted, or left behind.

-

Why Branding Matters for Smaller Businesses — and Why Investors Care

When most people hear the word “brand,” they think of global household names like Apple, Nike, or Virgin. These are companies with billion-dollar marketing budgets and armies of designers. But here’s the reality: for smaller businesses, brand is just as important, maybe even more so.

Why? Because in a crowded market where everyone claims to offer the same products or services, brand is the only way to stand out, earn trust, and build long-term value. And while large companies can afford to throw money at building recognition, SMEs have to be far more deliberate and strategic.

I often describe brand as the thread that ties everything together: your strategy, your people, your service, and your reputation. Without it, the business risks drifting. With it, everything lines up, customers know who you are, your team understands what you stand for, investors see the value, and growth becomes much easier to achieve.

Brand: More Than Just a Logo

One of the biggest misconceptions I see is that branding is just about visuals: a logo, a font, or a colour palette. Those are important, of course, but they’re the surface level. Brand goes much deeper.

True brand strategy starts with fundamental questions:

- What exactly does your business do? (Not just the service, but the real problem you solve.)

- Who are your customers? (What are their needs, fears, and aspirations?)

- Where are you going? (Your vision, mission, and values.)

The answers define your positioning in the market. They create the blueprint for how you communicate, the decisions you make, and how customers experience your business.

Get this right, and you’re consistent, credible, and memorable. Get it wrong, and you confuse the market, waste money on scattershot marketing, and weaken your ability to grow.

Investors Take Branding Seriously

Here’s something many SMEs don’t realise: investors care deeply about brand.

When an investor looks at a business, they’re not just looking at financials. They want to know:

- Does this company own a distinctive position in the market?

- Is the brand strong enough to attract customers without constant discounting?

- Can the team articulate a clear story to future buyers or partners?

- Does the company look, feel, and act like it’s investable and scalable?

I’ve seen investors walk away from perfectly solid businesses because the story wasn’t clear, the branding was inconsistent, or the market couldn’t easily understand what made them different.

Equally, I’ve seen the opposite: businesses with modest revenues but strong brands commanding far higher valuations, simply because the brand created trust, customer loyalty, and a believable path to growth.

Brand is one of those intangibles that directly affects tangible numbers: sales conversion, customer lifetime value, and even exit multiples.

Being On Brand Every Day

Here’s the critical point: a brand isn’t just a logo in a drawer or a strapline on your website. A brand is something you live every day.

It’s expressed through the way your sales team talks to prospects, how your operations team delivers, the language in your invoices, and even how your office feels when a client walks in. Every touchpoint is brand.

If your website claims innovation but your processes feel outdated, your brand promise collapses. If you tell the market you’re customer-first but fail to pay suppliers on time, you undermine your values.

This is why investors often push portfolio companies to get “on brand” internally as well as externally. They know that brand alignment across people, systems, and communications makes a company stronger, more scalable, and ultimately more valuable.

Why Many SMEs Struggle With Brand

Most small and mid-sized businesses struggle with branding for a few predictable reasons:

- They think it’s fluff. Many see brand as design work or marketing spin, rather than a commercial tool.

- They can’t articulate their story. Ask 5 people in the business what the company does best, and you’ll often get 5 different answers.

- They focus on short-term sales. Quick wins matter, but ignoring long-term positioning is a mistake.

- They lack in-house expertise. Without senior brand leadership, businesses end up muddling through.

The result? Inconsistent messaging, weaker differentiation, and a business that feels “small” even if its ambitions are big.

Thinking Long Term

Great branding isn’t just about this quarter’s sales. It’s about building an asset that compounds over years.

A strong brand should:

- Create trust with customers, suppliers, and partners.

- Attract talent — people want to work for businesses with a clear identity and reputation.

- Drive enterprise value — investors and acquirers consistently pay more for businesses with strong brands.

If you’re serious about scaling or exiting in the next 5–10 years, your brand equity will be one of the biggest drivers of valuation. It’s the story behind the numbers, and the difference between a business that sells for 4x earnings versus one that sells for 10x.

The Value of Fractional Branding Expertise

Not every business can justify hiring a full-time CMO or Head of Brand. But that doesn’t mean they should ignore brand. This is where fractional specialists come in.

A fractional brand consultant brings senior-level expertise without the full-time cost. More importantly, they bring objectivity. They can step back, assess how your business looks from the outside, and help you shape a clear, compelling identity.

Their role is to:

- Clarify your brand strategy.

- Align your people to it.

- Help you project it consistently into the market.

- Translate branding into commercial impact that investors will understand.

The best specialists also bring market benchmarks and proven processes. They know what works, what doesn’t, and how to implement branding that supports both operational delivery and valuation growth.

The Branding Journey

Most businesses that get serious about brand go through a fairly consistent process:

- Discovery & Audit – Review what exists today. How are you currently perceived?

- Brand Foundations – Define your vision, mission, values, and customer personas.

- Identity & Voice – Make sure design and language reflect strategy.

- Embed the Brand – Train and align staff so everyone is consistent.

- Projection – Apply brand to websites, social channels, mailshots, events, PR.

- Evolution – Review and adapt as the market and business change.

The key is consistency. Whether a prospect finds you on LinkedIn, meets you at a conference, or calls your office, the experience should always feel aligned.

Final Thought

For SMEs, brand is often underestimated. Yet it can be the single biggest lever for growth, differentiation, and long-term value.

Branding isn’t about looking pretty. It’s about clarity, consistency, and confidence. It’s about living your values, standing out in the market, and building trust with every interaction.

Investors know this. It’s why they scrutinise brand in due diligence, and why they often bring in specialists to fix it. Done well, branding transforms not only how you’re seen, but also how you perform.

Brand is not a cost. It’s an asset. And for smaller businesses, it’s the difference between being “just another player”, or being the business that everyone wants to back, buy from, and invest in.

-

Why Founders Often Get Their Investment Ask Wrong — and How to Get it Right

By Anthony King, Founder at Kognise

Raising investment is one of the most high-stakes, high-visibility activities a founder will ever face. And yet, one of the most common, and costly, mistakes in early-stage fundraising happens before the first pitch is even delivered: the size of the ask.

Too high, and you risk scaring off investors with unrealistic valuations. Too low, and you undercut your own growth, appearing naive, underprepared, or worse, unscalable.

At Kognise, we specialise in helping founders sharpen their commercial story and translate vision into investible propositions. That means digging deep into the strategic logic behind “how much are you raising?”, and turning that ask into an asset, not a liability.

Common Mistakes When Calculating the Ask

1. Asking for Too Little (The Undershoot Trap)

Many founders take a conservative approach, thinking a smaller number makes their business more attractive. But seasoned investors see this for what it often is: a lack of confidence, clarity, or commercial depth.Low asks can also damage credibility, as if the founder hasn’t done their homework. A SeedLegals survey showed that the average UK seed round in 2024 was £685K, up from £535K in 2022. Investors benchmark against this. Fall too far below, and they start asking hard questions.

2. Raising Based on Time, Not Milestones

Founders often say, “We’re raising 12 months of runway.” But smart investors fund outcomes, not time.A more compelling approach is milestone-based planning. What tangible progress can you achieve with this raise that de-risks the next stage?

For example:

- Proptech startup Nested raised £5M to complete a regulated mortgage product and secure its first 50 clients.

- CarbonChain focused its $10M raise on building its emissions tracking platform for the shipping and steel sectors.

In both cases, investors backed acceleration, not just survival.

3. Ignoring the Link Between Ask and Valuation

Founders frequently propose numbers that don’t align with their proposed valuation or traction. For example: raising £2M at a £4M pre-money valuation with no revenues, or raising £250K while offering just 1.5% equity.This mismatch raises red flags. According to Beauhurst, the median UK startup valuation at Seed stage in 2023 was £6.5M. If your traction doesn’t match that, or your raise-to-equity ratio is off, you risk undermining investor trust.

Your raise must make sense within your overall capital plan:

- What equity are you giving up now?

- What will be left for future rounds?

- How does it tie to the company’s growth trajectory?

A Better Way to Calculate Your Ask

At Kognise, we guide founders through a more strategic, evidence-based method.

Step 1: Start with Outcomes

List your top three to five key business milestones for the next 12–18 months. These might include:- Completing MVP development

- Achieving regulatory approvals

- Securing a set number of customers

- Hitting a monthly recurring revenue target

- Building a senior team or sales engine

Each milestone should directly reduce risk and increase valuation at your next round.

Step 2: Build a Budget Backwards

Rather than arbitrarily choosing a number, construct your raise based on the actual costs of achieving those milestones. That includes:- Salaries (founders, tech, ops, sales)

- Marketing and customer acquisition

- Product development and infrastructure

- Legal, IP, or compliance

- Cash buffer for unexpected challenges

Be realistic. Most founders underestimate hiring costs and timelines. Investors know this. If your plan doesn’t reflect actual hiring timelines and market rates, you’ll be marked down.

Step 3: Fit the Raise to the Round Type

Your ask should reflect where you are. Here’s a simplified guide based on UK funding norms:Stage Typical Raise What’s Expected Pre-seed £150K–£500K MVP, early proof of concept Seed £500K–£2M Product in market, early traction, go-to-market clarity Series A £2M–£10M+ Commercial growth, repeatable sales, team in place If your ask falls outside these bands, you’ll need an exceptional story (e.g. deep tech, regulated markets, strategic IP).

Step 4: Link to Valuation and Dilution

Ensure your raise makes sense relative to the equity you’re offering. If you’re raising £1M and offering 10%, that implies a £9M pre-money valuation. Are you ready to justify that?Real-World Insight: What Investors Actually Want

Investors don’t expect your plan to be perfect — but they do expect it to be coherent.

A well-structured ask signals:

- That you understand your business

- That you’ve done the work to de-risk it

- That you’re raising the right amount — not the most you can get

Investors like MMC Ventures, LocalGlobe, or Octopus Ventures often say that the best pitches come from founders who clearly link capital to growth logic. They want to see your business expand value, not just extend life.

How Kognise Helps

We work hands-on with founders to reshape their pitch, deck, and data room — but more than that, we help define the right size and structure of the raise.

That means:

- Milestone modelling: aligning your capital plan with tangible outcomes

- Investor alignment: matching raise and equity to stage-specific expectations

- Narrative clarity: turning your commercial plan into a compelling investor story

Whether you’re raising £300K or £3M, your ask is a window into your credibility. If it’s vague, underpowered, or misaligned, the door may close before the meeting even starts.

Final Thought

Fundraising isn’t just about storytelling, it’s about financial and strategic precision. The right ask, built on logic, confidence, and credible growth levers, turns capital into momentum.

If you’re unsure whether your raise stacks up, or how it will land with investors, Kognise can help you sense-check, shape, and strengthen your investment case.

-

High Profile Deals, Billion-Pound Funds and Everything in Between

Why our work at Kognise is anything but boring

We’re often asked what we actually do at Kognise. It’s a fair question, because no two weeks, or even two days, ever look quite the same. And that’s exactly how we’ve built it.

One moment, we’re elbows-deep in the operations of a sustainability-focused business, we’re there not just as advisors, but as temporary partners—fixing what’s broken, simplifying what’s overbuilt, and ensuring the business can find its feet and move forward with confidence.

Then, almost in the same breath, we’re sat across the table from a team managing over £100 billion in global real assets, walking through long-horizon investment theses and mapping out capital strategies that align social impact, sustainability, and serious commercial return. Often, we’re not just helping them deploy, but co-creating new vehicles, platforms or strategies that don’t exist yet.

That same week, we might be on Zoom with a globally known star from the film industry and their team, exploring how to develop their sport and wellness brand and space. Or we’re on the phone with one of the biggest names in global entertainment, building a roadmap for how they can use clean technology to decarbonise how they create, perform and engage with millions of fans worldwide.

This is the range. And this is the energy. It’s varied, it’s unpredictable, and frankly, it’s the reason we get up in the morning.

At any given time, we’re working with companies across the capital stack—pre-funding, post-raise, or in full-blown distress. Some founders come to us looking to raise smart capital with the right structures behind it. Others are scaling fast and know they need help building around the momentum. And some, quite frankly, are in triage mode. The business is burning too hot, the board’s getting nervous, or the strategic clarity’s just gone missing.

Whatever the situation, our role is consistent: structure, calm, capital, and momentum. Whether that’s stepping in operationally, supporting the raise, or reshaping the model for what comes next, we get in fast and build forward from wherever the business is today.

We work best where there’s a blend of ambition, complexity, and commercial potential. Sometimes, it’s a first-time founder with a world-class product and no idea how to commercialise it. Other times, it’s a well-resourced PE house looking to bolt on a strategic acquisition and turn it into something investable. We’ve helped pharma clients bring their IP to market, worked with media and sports groups to rethink their entire monetisation model, and helped turn cultural assets into scalable businesses.

The sectors vary—often wildly. But what stays constant is our approach: get clarity, take action, and deliver results. No fluff. No decks for the sake of it. Just focused work that makes things happen.

Right now, we’re speaking to a number of billion-pound impact funds and family offices who are actively looking for differentiated deal flow, credible co-investment opportunities, and the kind of projects that sit outside the standard PE conveyor belt. We’re also working with operators who are building the next wave of growth in markets that matter—sustainable infrastructure, agri-tech, digital health, future of sport, entertainment IP and more.

And the timing matters. The market is shifting hard. Sustainable investment now tops £30 trillion globally. Private equity dry powder is at all-time highs—£2.8 trillion and counting. At the same time, UK insolvencies are up 44% year-on-year, and the pool of distressed but high-potential businesses is only growing. It’s a rare window where smart capital, sharp execution, and real vision can create meaningful, asymmetric outcomes.

At Kognise, we’re not here to make things look good—we’re here to make them work. We go deep, move fast, and operate side-by-side with people who are building, fixing, or reimagining something meaningful. From board-level strategy to front-line delivery, we match ambition with action—and we’re always up for a challenge.

If you’re building something exciting, need help stabilising or scaling, or simply want access to distinctive deal flow—we should talk.