-

Why Do So Many Funded Businesses Still Fail?

Perhaps we’ve been asking the wrong questions for decades.

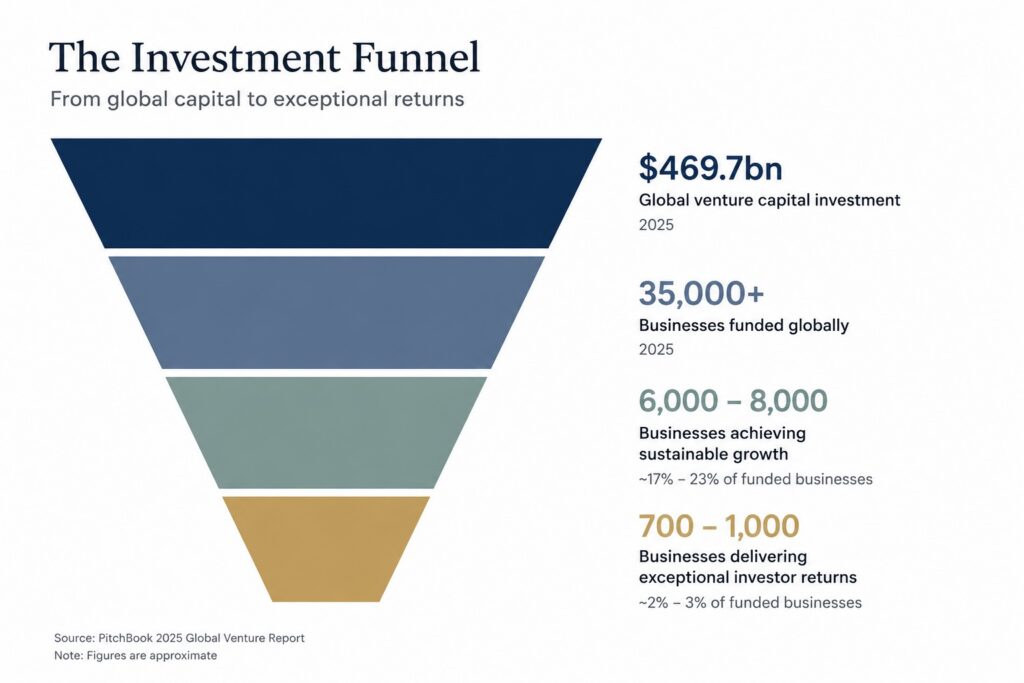

Global venture capital investment recovered strongly during 2025, with almost US$470 billion invested into growth businesses worldwide following the market correction of the previous two years. Thousands of companies secured funding from venture capital firms, family offices, private equity investors and angel networks, each having passed through detailed financial analysis, legal review, commercial assessment and investment committee scrutiny. Yet despite increasingly sophisticated investment processes and unprecedented access to market intelligence, the pattern of outcomes remains remarkably familiar. A relatively small proportion of funded businesses generate exceptional returns, many achieve only modest growth and a significant number fail to deliver the value that investors originally expected. The investment community has become better equipped, better informed and better connected than at any point in its history, but identifying tomorrow’s outstanding businesses remains as challenging as ever.

Risk is, and always will be, an inherent part of investing. Every experienced investor understands that exceptional returns are only possible because uncertainty exists, and no process will ever eliminate that uncertainty entirely. The more interesting question is whether our methods of assessing businesses have evolved at the same pace as the businesses themselves. Modern investors have access to real-time operational data, sophisticated financial modelling, artificial intelligence, global market intelligence and collaborative digital data rooms that previous generations could scarcely have imagined. If the tools available to us have transformed so dramatically, why do investment outcomes continue to follow much the same pattern they always have?

Perhaps the answer is not that investing is inherently unpredictable. Perhaps we have become exceptionally good at answering the questions that defined investment fifty years ago, whilst giving far less attention to the questions that will define successful investment over the next fifty.

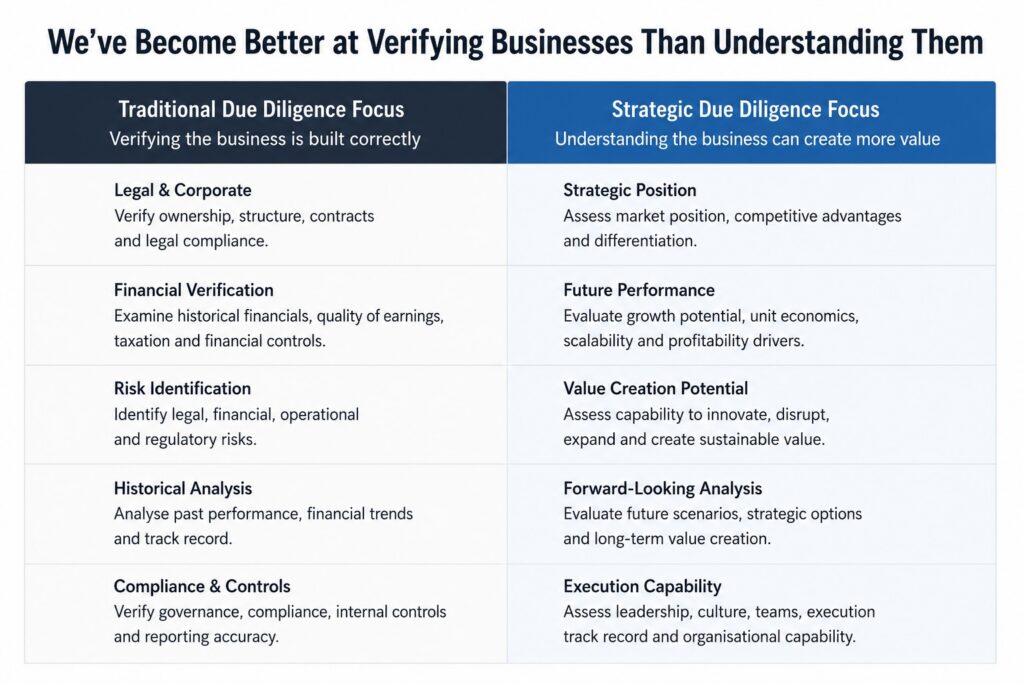

The way we assess businesses today has its roots in a very different commercial world. Long before cloud platforms, virtual data rooms and financial modelling software, companies existed largely on paper. Contracts were stored in filing cabinets, statutory records occupied archive rooms and financial information was maintained in physical ledgers. During acquisitions and investment rounds, potential investors were often granted controlled access to these records so they could verify ownership, examine financial performance and identify legal or commercial risks before committing capital. In that environment, due diligence was exactly the right process because the records represented the business itself, and confidence in those records was fundamental to making an informed investment decision.

Business has changed dramatically since then. Financial information is now updated continuously rather than annually, customer relationships are managed through cloud-based systems, product development is planned years ahead using digital roadmaps and sophisticated financial models can evaluate multiple commercial scenarios in minutes rather than weeks. Increasingly, the value of a business is derived not from its physical assets but from intellectual property, recurring revenue, proprietary technology, data and the capability of its people to innovate and execute. We have transformed almost every aspect of how businesses operate, yet the underlying philosophy of investment assessment remains remarkably familiar. We still devote enormous effort to verifying that a business has been built correctly, but comparatively little to understanding whether it possesses the characteristics required to become substantially more valuable over time.

That distinction is important because investors are not committing capital simply because the paperwork is accurate or the accounts reconcile. They invest because they believe the business has the capability to create significantly more value in the future than exists today. Verification remains essential because every investment must be built upon solid foundations, but confidence in the foundations alone has never created an investment return. At some point, every investor must move beyond asking whether the business is genuine and begin asking whether it is genuinely capable of creating value.

Enterprise Value Is Created, Not Calculated

None of this diminishes the importance of traditional due diligence. Investors should continue to examine legal structures, financial controls, intellectual property, taxation, regulatory compliance and governance because weaknesses in any of these areas can materially affect the value of an investment. The discipline has evolved over many decades for good reason, and it remains an essential part of protecting investors from unnecessary risk. The question is not whether these activities should continue, but whether they answer the question that investors are ultimately trying to resolve.

Once the legal documentation has been reviewed and the financial records verified, the conversation around almost every investment begins to change. Investment committees start discussing the capability of the management team, the credibility of the commercial strategy, the realism of the financial forecasts, the size of the addressable market and the competitive position of the business. They debate whether the product roadmap is sufficiently differentiated, whether the sales assumptions are achievable and whether the business has the operational maturity to scale. These discussions are often where investment decisions are ultimately won or lost, yet they tend to sit outside the traditional valuation process despite being the very factors that determine whether a business creates significant enterprise value.

Perhaps that is where our thinking should begin to evolve. Rather than viewing due diligence, financial forecasting, commercial analysis and valuation as separate exercises, they can instead be seen as different perspectives on exactly the same objective. Each contributes evidence towards understanding whether a business possesses the capability to grow, adapt, compete and create value over time. None of them, in isolation, answers that question particularly well, but together they begin to form a far richer picture than a valuation or due diligence report can provide independently.

Investors Don’t Buy Today’s Business

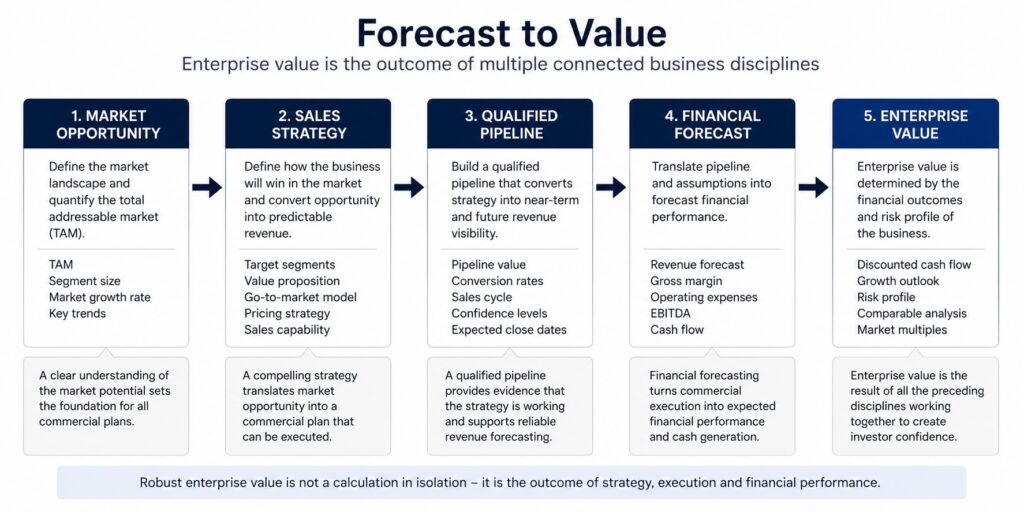

One of the most common questions asked by founders preparing for investment is, “What is my business worth?” It is an entirely understandable question because a valuation often becomes the focal point of a funding round. Negotiations revolve around pre-money and post-money valuations, ownership percentages and dilution, leading many founders to view valuation as the objective rather than the outcome. Investors, however, are rarely buying today’s business, they are buying the business they believe it can become.

That distinction is subtle, but it changes almost everything. A valuation is not simply a mathematical exercise applied to a financial model; it is an expression of confidence in the future. Investors commit capital because they believe the business will execute its strategy, grow its revenues, improve profitability, strengthen its competitive position and ultimately become significantly more valuable than it is today. Every assumption embedded within a financial model is, therefore, a statement about future value creation rather than a reflection of historic performance.

Seen through that lens, valuation becomes less about calculating a number and more about understanding the drivers behind it. A sales forecast has little meaning unless it is supported by a credible route to market. Revenue projections carry limited value unless they are underpinned by qualified opportunities and realistic conversion assumptions. Likewise, product roadmaps matter not because they look impressive in an investor presentation, but because they demonstrate how future innovation will expand markets, strengthen competitive advantage or reduce the cost of delivering products and services. Even the management team becomes part of the valuation discussion because great businesses are rarely built by financial models alone; they are built by capable people making consistently good decisions.

This is where many traditional valuation exercises begin to show their limitations. They often capture the outputs of these activities without fully assessing the quality of the inputs that produced them. Two businesses may present identical financial forecasts whilst having entirely different probabilities of delivering them. One may have a highly qualified sales pipeline, a clearly differentiated product strategy and a proven management team with deep sector expertise. The other may rely on optimistic assumptions, an untested proposition and limited evidence that demand genuinely exists. The valuation models may appear remarkably similar, but the businesses themselves are fundamentally different because their capacity to create future value is fundamentally different.

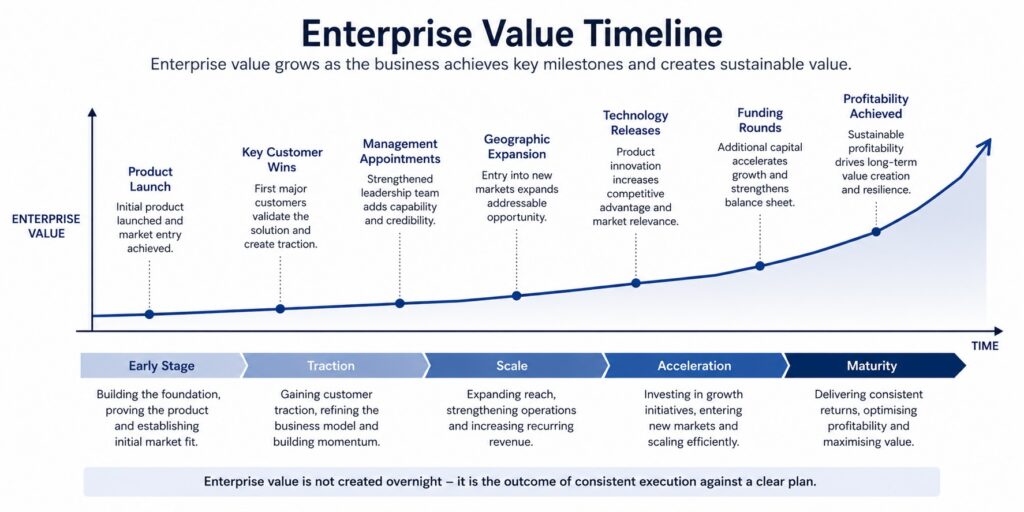

Enterprise Value Should Never Stand Still

Every successful business continually revises its understanding of the future. Sales forecasts evolve as opportunities are won and lost, financial models are updated as assumptions change and product roadmaps adapt in response to customer feedback, technological advances and competitive pressure. Strategy itself is never static because markets are constantly moving, and boards rightly expect management teams to respond to those changes.

Valuation rarely enjoys the same treatment. In many organisations it remains an event rather than a management discipline, produced to support fundraising, acquisition or shareholder discussions before quietly becoming a historical document until the next transaction. Yet every decision made by the board has the potential to increase or decrease enterprise value. Winning a strategic customer, strengthening the management team, entering a new market, launching a differentiated product or improving operational efficiency all change the future trajectory of the business. Equally, losing market share, delaying product development or weakening commercial performance reduces that trajectory. If these changes are continually reshaping the business, it seems increasingly difficult to justify assessing enterprise value only at isolated points in time.

Perhaps the opportunity is not to replace due diligence or reinvent valuation methodologies, but to recognise that both should form part of a broader understanding of how businesses create value. Rather than treating enterprise value as the destination, it becomes another management metric alongside revenue, profitability, cash flow and customer growth. That subtle shift changes the role of valuation from a number used to support fundraising into a strategic tool that helps founders and investors understand whether the business is moving in the right direction—and, more importantly, why.

A Better Question Creates Better Decisions

Every investment ultimately comes down to a judgement about the future. The legal review, financial analysis, commercial assessment and valuation all exist to reduce uncertainty, but none of them can remove it entirely. At some point, every investor has to decide whether they believe this business is capable of becoming significantly more valuable than it is today. That decision is based less on historic performance than on confidence in the organisation’s ability to execute its strategy, adapt to changing markets and consistently create value over time.

That is precisely why founders and investors are far more closely aligned than they often realise. Founders want to build valuable businesses because that is how they create wealth for themselves and their shareholders. Investors want those businesses to become substantially more valuable because that is how investment returns are generated. Both parties are therefore pursuing exactly the same objective. The difference is that founders frequently view valuation as an event associated with fundraising, whilst investors view it as the expected outcome of a successful business. Reframing valuation as a continuous measure of enterprise value rather than a point-in-time calculation creates a common language that benefits both.

This also changes the role of business planning. Financial forecasts become more than projections of revenue and profitability; they become evidence supporting future enterprise value. Sales forecasts are no longer simply ambitious targets but qualified assessments of commercial opportunity, supported by realistic assumptions around conversion, customer acquisition and market demand. Product roadmaps become more than lists of future features because they demonstrate how innovation is expected to strengthen competitive advantage, expand addressable markets or reduce operational costs. Every major strategic decision begins to contribute directly towards understanding whether the business is becoming more valuable and, just as importantly, why.

This broader perspective has another significant advantage. Traditional due diligence often identifies weaknesses immediately before investment, when opportunities to address them are limited by time and transaction pressures. A more continuous assessment encourages those same issues to be identified much earlier, giving founders the opportunity to strengthen the business before entering a funding process. Investors benefit from a more resilient investment opportunity, whilst founders benefit from building a stronger business irrespective of whether external funding proceeds. The process moves from identifying problems at the point of investment towards improving businesses throughout their growth journey.

Looking Beyond Traditional Due Diligence

The intention is not to dismiss the principles that have underpinned investment for decades. Due diligence remains fundamental because investors deserve confidence that a business has been built upon solid foundations. Equally, established valuation methodologies remain valuable because they provide recognised approaches for assessing value from different financial perspectives. Those disciplines have stood the test of time and will continue to play an important role in investment decision-making.

What deserves greater discussion is the objective those disciplines are trying to achieve. If the ultimate purpose of investment assessment is to identify businesses capable of creating exceptional long-term value, then perhaps our processes should become more explicitly focused on answering that question. Rather than viewing due diligence as the destination and valuation as the conclusion, they become complementary components within a broader assessment of enterprise value. The emphasis shifts from verifying what the business is today towards understanding what it is capable of becoming.

This is the thinking that has shaped our work at Kognise. Rather than treating valuation as a standalone financial exercise, we increasingly view it as the natural outcome of understanding a business in its entirety. Market opportunity, commercial execution, qualified sales forecasts, financial modelling, operational maturity, governance, leadership capability and innovation all contribute to enterprise value, and their interaction often reveals far more than any single report can achieve independently. The objective is not to produce longer due diligence reports or increasingly complex valuation models; it is to provide founders and investors with a clearer understanding of the factors that genuinely influence the future value of a business.

Perhaps that represents evolution rather than revolution. The investment industry has continually adapted to new markets, technologies and commercial models, yet many of the underlying questions have remained remarkably consistent. As businesses become increasingly dynamic, data-driven and technology-enabled, there is an opportunity to rethink not the principles of investment assessment but the purpose behind them. Asking whether a business is genuine will always remain important. It is simply no longer sufficient on its own.

The more valuable question may be whether the business possesses the capability to create sustained enterprise value.

If that becomes the question we ask first, founders gain a clearer understanding of what drives the value of their business, investors gain greater confidence in the direction of travel rather than simply a snapshot in time, and the conversation moves beyond fundraising towards building stronger, more valuable companies.

Ultimately, successful investing has never been about finding businesses that simply survive scrutiny. It has always been about identifying businesses capable of creating extraordinary value.

Perhaps it is time that our approach to investment assessment reflected exactly that.

Author’s Note

This article introduces the principles behind the Kognise Enterprise Value Assessment™ (KEVA™) methodology. Developed by Kognise to complement traditional due diligence and valuation, KEVA™ provides a structured approach to assessing an organisation’s capacity to create long-term enterprise value by integrating commercial, strategic, operational, governance and financial disciplines into a single enterprise assessment.

Rather than viewing due diligence, commercial analysis, financial modelling and valuation as separate activities, KEVA™ considers how these disciplines interact to influence an organisation’s future enterprise value. The methodology continues to evolve through its application across investment, fundraising and corporate advisory engagements.

Constructive discussion with founders, investors, corporate finance advisers and fellow practitioners is welcomed as part of that ongoing development.

-

Cheshire and Warrington Growth HUB – Cheshire Business Angels Pitch Day – Wednesday 10th June

Had a great day at Chester Racecourse today as a guest of the Cheshire and Warrington Growth Hub

Richard Lydon presenting The morning began with insightful presentations from my good friend Pete Loughlin of Xeinadin and Gorvins Solicitors, followed by an engaging session from Deepbridge Capital and my colleague Richard Lydon on what investors are really looking for when assessing new opportunities.

The afternoon focused on a series of pitches from innovative businesses seeking investment, followed by lunch and the opportunity for some excellent informal conversations with founders, investors and advisers alike, some of which I have worked with so it was a good opportunity to catch up.

Chester racecourse Trophy Cabinet To round off the day, Kate Dawson, Commercial Director at Chester Racecourse, gave us a fascinating tour of the racecourse, sharing its rich history and exciting plans for the future.

A well-organised event, some strong businesses, and plenty of interesting conversations throughout the day.

-

The Founder Equation: Why Teams, Personal Alignment and Human Reality Matter More Than the Product

Over the course of my career I have worked across everything from institutional venture-backed businesses through to UHNW and Family Office backed projects where funding decisions could happen in weeks rather than over multiple investment committee cycles stretching across months.

The environments, structures and timelines were often very different, but one thing remained remarkably consistent throughout: the people behind the business were usually the deciding factor.

I have seen technically brilliant products fail because the founders could not execute commercially, could not build teams around themselves, could not adapt under pressure or simply burned themselves and everyone around them out. Equally, I have seen comparatively average or incomplete products become highly successful because the founders were disciplined, resilient, commercially self-aware and capable of building strong teams around them.

One of the clearest examples for me personally was turning down involvement in a project associated with Nolan Bushnell, Atari founder and Steve Jobs’ first employer. Nolan is hugely charismatic and the project itself had enormous profile attached to it. Instead, I chose to back a deeply troubled business carrying substantial debt and operational pressure because the founder demonstrated something far more important to me: resilience, realism, accountability and the ability to execute under pressure.

That reinforced something I had already begun to understand years earlier. Products matter, technology matters and markets matter, but over time the quality, stability and adaptability of the people behind the business usually become the determining factor.

There is a persistent myth in the start-up ecosystem that great products inevitably win. They do not.

Markets are full of technically brilliant products that failed commercially, while comparatively average products built by disciplined, resilient and commercially aligned teams became category leaders. The uncomfortable reality for many founders is that this shifts the focus away from the product itself and onto the people building it. Investors know this. Experienced operators know this. Most failed founders eventually realise it.

A start-up is not simply a product. It is a living system of people, decision-making, resilience, communication, compromise, timing, leadership, emotional control, operational execution and commercial discipline. The best product in the world will fail if the people behind it cannot execute.

Equally, an exceptional team can often evolve, reposition, simplify or commercialise a mediocre product into a highly successful business. This is why sophisticated investors spend as much time assessing founders, leadership dynamics and operational maturity as they do assessing technology.

The Market Reality: Most Start-Ups Fail

The statistics surrounding start-up failure are widely discussed, but often poorly understood. According to data from the US Bureau of Labor Statistics, approximately 20% of new businesses fail within the first year, around 50% fail within five years, and close to 65% fail within ten years.

CB Insights, in one of the most widely cited studies on venture-backed start-ups, identified the leading causes of failure as:

- No market need

- Running out of cash

- Wrong team

- Poor pricing/cost structure

- Product mistiming

- Internal conflict

- Loss of focus

- Burnout

- Failure to pivot

Interestingly, very few failures occur because the product itself was technically impossible. Failure is usually caused by poor execution, weak leadership, co-founder conflict, inability to scale operations, poor hiring, emotional instability under pressure or founders simply exhausting themselves mentally and physically.

This is one of the reasons venture capital firms often invest in founders before products. A great team can identify market changes, reposition the offer, attract talent, secure investment, survive setbacks and evolve the product over time. A weak or dysfunctional team cannot.

Investors Rarely Back Products Alone

Founders often believe investors primarily fund ideas. Most experienced investors do not.

At early stage, investors are usually backing founder capability, resilience, communication, adaptability, operational awareness, commercial realism and the team’s ability to execute under pressure. This becomes increasingly obvious during difficult market conditions.

During the technology downturn between 2022 and 2024, many businesses with substantial funding and technically impressive products failed because they had overhired, misunderstood demand, scaled too early or lacked operational discipline. In many cases the founders were simply unable to transition from “builder mode” into company leadership.

In contrast, many smaller businesses survived because they had disciplined cash management, adaptable leadership, lean operating structures and emotionally stable founders. Execution almost always beats theory.

Great Teams Beating Better Products

Instagram was not the first photo-sharing application, nor was it technically the most sophisticated. Competitors already existed with larger feature sets and stronger engineering capability. What Instagram had was simplicity, clarity of positioning, disciplined product focus and a highly adaptive founding team.

The founders recognised very early that users preferred the photo functionality over the broader product they originally launched as “Burbn”. Instead of defending their original vision, they pivoted aggressively. That decision changed the trajectory of the company.

Slack provides another example. The company emerged from the collapse of a gaming business. The original business failed, but the internal communication tool built by the team proved more valuable than the original product. Many founders would have continued chasing the original vision. Instead, the leadership team recognised where the market pull actually existed and repositioned the company.

Apple is often cited as a product company, but its long-term success came from obsessive operational execution, leadership clarity and cross-functional alignment. Many companies had products technically comparable to Apple’s. Very few had the same design discipline, ecosystem thinking and operational coordination.

The opposite lesson can be seen in WeWork. The business had huge investment, rapid growth and a compelling narrative, but governance, leadership discipline and operational realism failed to mature at the same pace. The issue was not that office space was impossible as a business. The issue was leadership structure, financial control and strategic realism.

The Most Dangerous Founder Assumption

One of the biggest mistakes founders make is assuming that if the product is good enough, everything else will work itself out. Usually the opposite is true.

As a company scales, communication becomes harder, operational complexity increases, investor expectations rise, hiring becomes critical and founder emotional resilience gets tested constantly. The product often becomes the easiest part. The human systems become the hardest.

Many start-ups fail because founders never properly discussed ambition, lifestyle expectations, risk tolerance, compensation, family plans, exit expectations or long-term personal goals.

At the beginning of a company everyone is optimistic. Three years later, one founder may want aggressive scaling while another wants stability. One may want venture capital while another fears dilution. One may want international expansion while another is dealing with young children and family pressures.

If these conversations never happened properly, conflict becomes inevitable.

Founders Must Build Businesses Around Human Reality

One of the least discussed areas in entrepreneurship is the importance of integrating personal reality into strategic planning. Founders are often encouraged to sacrifice everything, work constantly and ignore personal life. Publicly this is celebrated. Privately it destroys relationships, health, decision-making and sometimes the business itself.

A founder with young children, caring responsibilities, family health pressures or major personal goals cannot simply pretend these things do not exist. Nor should they.

Sophisticated founders build businesses acknowledging reality rather than denying it. Good investors quietly assess founder stability, emotional resilience, burnout risk, leadership maturity and operational sustainability because founder instability destroys businesses.

Investors have repeatedly seen divorces derail companies, burnout destroy decision-making, founder conflict kill momentum and unmanaged personal pressures create operational chaos. A founder pretending to be invincible is usually a risk. A founder who understands their constraints and builds intelligently around them is often far safer.

Personal Plans Matter More Than Founders Admit

Founders frequently build business plans assuming unlimited availability, energy and emotional capacity. That is rarely realistic.

Questions founders should ask themselves include:

- Do I want children during the next five years?

- Am I prepared for constant travel?

- How much financial pressure can my family absorb?

- What does success actually look like personally?

- What am I unwilling to sacrifice?

- Do I want a venture-backed hypergrowth business or a profitable controlled company?

These are not soft questions. They directly affect leadership capacity, hiring strategy, capital requirements, growth pace and investor suitability.

The best founders build structures that reduce dependency on themselves. This includes delegating early, hiring complementary people, building leadership depth, documenting processes and creating operational resilience.

Too many start-ups are effectively one exhausted founder holding the entire business together. That is not scalable and it is not investable long term.

If a founder knows they want flexibility, family time or periods away from the business, the answer is not necessarily to work harder. The answer may be stronger leadership hires, better governance, improved delegation or slower, healthier scaling.

The Importance of Transparency with Investors

Many founders fear discussing personal realities with investors. In reality, sophisticated investors usually appreciate honesty and self-awareness.

What concerns investors is not founders being human. It is founders hiding risks, lacking self-awareness, overpromising or building businesses entirely dependent on unsustainable behaviour.

A founder saying “I have young children and therefore I am building a management structure that reduces founder dependency over time” is often viewed far more positively than someone insisting they can personally do everything indefinitely.

Over the past decade there has been increasing recognition that burnout damages performance, toxic founder culture destroys retention and hypergrowth at any cost is dangerous. Markets now place far greater value on governance, operational maturity, sustainable scaling and leadership stability.

This is particularly visible in sectors such as climate technology, infrastructure, enterprise software, healthcare and financial services where operational resilience matters enormously.

Building a Company Is Ultimately a Human Exercise

Technology matters. Products matter. Markets matter. But businesses are ultimately built by people.

The ability to lead teams, manage conflict, adapt under pressure, maintain clarity, attract talent and build resilient structures often determines success far more than the product itself.

A mediocre product with exceptional execution, strong culture, disciplined leadership and adaptive founders can become extremely successful. An excellent product with poor leadership, founder conflict, burnout and weak governance usually struggles eventually.

The start-up ecosystem often celebrates the product. Experienced operators understand the real asset is usually the people behind it.

The founders who build with awareness of both commercial reality and human reality are often the ones who create businesses capable not only of scaling — but surviving.

-

Most Businesses Don’t Have A Funding Problem. They Have A Funding Strategy Problem!

One of the most common mistakes we see at Kognise is businesses jumping into fundraising before they have properly worked out what they actually need, why they need it and what type of capital is genuinely appropriate for the stage they are at.

Founders often start with a headline number:

“We need £2m.”

“We are raising £5m.”

“We need bridge funding.”But once you start working backwards through the operational plan, the hiring assumptions, the sales cycle, the technology roadmap, infrastructure requirements and runway assumptions, the numbers often change quite dramatically. In many cases the original ask was either too small to genuinely achieve the stated objectives or unnecessarily large for the stage the business had actually reached.

Raising capital should never really start with the valuation, the investor list or even the deck itself. It should start with understanding what the business is genuinely trying to achieve over the next 18–36 months and what resources are realistically required to get there.

In practice, most growth requirements break down into a combination of:

- equity,

- lending,

- operational expertise,

- strategic relationships,

- and market access.

The problem is that many businesses default straight to equity because it is the most visible form of fundraising, even when significant parts of the requirement could potentially be solved through structured lending, asset finance, strategic partnerships or specialist operators who can materially accelerate the business.

We see this regularly in infrastructure-heavy or hardware-led businesses where founders are trying to fund operational assets entirely through equity when parts of the requirement may sit far more naturally within lending or asset-backed finance structures. The same applies to inventory-heavy businesses, international expansion projects and working capital requirements where excessive dilution can happen surprisingly quickly if every operational challenge is solved through founder equity.

Understanding that distinction matters because the wrong funding structure can create problems that remain embedded in the business for years.

The wider funding environment itself has also changed significantly. PitchBook data showed US VC deal value exceeding $267bn in Q1 2026, but a very large proportion of that capital was concentrated into a relatively small number of AI and infrastructure-related transactions. Strip out the mega-rounds and the underlying market looks materially tighter than many headlines suggest, which is one of the reasons staged funding is becoming increasingly important.

Investors now want to see measurable progression underneath the story before committing larger amounts of capital. In practical terms that usually means businesses moving through a series of gates:

- technical validation,

- prototype completion,

- early commercial traction,

- regulatory milestones,

- customer adoption,

- recurring revenue,

- operational scaling,

- or international expansion.

Each stage effectively de-risks the next one because investors can see tangible evidence of progression rather than simply funding future ambition based purely on forecasts and narrative.

In reality, many of the strongest businesses scale funding requirements over time rather than trying to raise one enormous round too early. Founder and angel capital may validate the concept, seed funding may build the product and early traction, then larger growth rounds support scaling and infrastructure deployment once the operational foundations underneath the business are more mature.

Where businesses often get themselves into difficulty is trying to jump too far ahead of their actual level of operational readiness. Investors may absolutely believe in the long-term opportunity whilst simultaneously concluding that the business has not yet demonstrated enough evidence to absorb that level of capital effectively.

The opposite problem exists as well, particularly in tougher markets, where businesses quietly end up trapped in survival fundraising. We increasingly see companies raising:

- £50k here,

- £100k there,

- another bridge round,

- another short-term note,

- another emergency extension,

simply to keep operating whilst no wider strategic funding plan exists underneath it.

Over time the cap table becomes fragmented, founder dilution accelerates, governance becomes messy and institutional investors start seeing operational instability rather than strategic progression. Internally founders often describe this as “keeping the lights on”, but investors usually interpret repeated small rescues very differently.

Carta data recently showed bridge rounds accounting for around 16.6% of all startup cash raised on its platform during 2025, which gives some indication of how many businesses are now extending runway rather than progressing cleanly into larger institutional rounds. Investors understand why this is happening, but repeated small rescues without meaningful progression underneath them can quickly become a red flag.

Another area founders consistently underestimate is intellectual property, particularly in AI and software markets where barriers to entry are collapsing quickly and investors are increasingly trying to understand what genuinely creates defensibility underneath the business.

A surprising number of businesses still cannot clearly explain:

- what IP they actually own,

- where it legally sits,

- whether contractor assignments are properly documented,

- how protected it really is,

- or what genuinely creates a competitive moat against better-funded competitors.

A few years ago broad technology positioning itself could often attract investor excitement. Increasingly investors now want to understand:

- proprietary data,

- licensing structures,

- operational integration,

- patents,

- ecosystem positioning,

- and whether larger competitors could realistically replicate the product within a relatively short timeframe.

This is one of the reasons IP holding companies have become increasingly common, particularly in software, platform and internationally scaling businesses. In simple terms, the IP HoldCo owns the intellectual property and licenses it into operating businesses underneath it, which can create genuine strategic advantages around:

- clearer ownership,

- separation of trading liabilities,

- international licensing flexibility,

- acquisition structuring,

- and stronger long-term protection of core assets.

However, this is also an area where founders can create very serious problems if handled badly because moving IP between entities can trigger:

- tax consequences,

- transfer pricing issues,

- valuation disputes,

- financing complications,

- and shareholder concerns.

If external investors already exist, poorly handled IP movement can undermine confidence extremely quickly, particularly if investors feel valuable assets are being moved without proper governance or commercial rationale underneath it. This is why IP structuring should never be approached casually or copied from generic founder content online. Proper legal, tax and commercial advice matters because mistakes here can become extremely expensive later.

The same thing applies to investor outreach itself. One of the more frustrating trends over the last few years has been the explosion of LinkedIn posts offering:

- VC databases,

- investor email lists,

- “10,000 active investors”,

- and mass outreach templates,

most of which are close to worthless once you understand how investment firms actually behave internally.

Professional investors are already inundated with cold decks and generic outreach. Founders often massively underestimate how much noise funds already receive, particularly in popular sectors such as AI, climate and SaaS. Generic outreach to random analyst or associate inboxes rarely creates meaningful engagement unless the opportunity is exceptionally well aligned or already carrying strong momentum.

More importantly, most founders do not properly understand that funds themselves operate in cycles. You need to know:

- whether the fund is actively deploying,

- what stage they invest at,

- whether reserves are already committed,

- what sectors they are prioritising,

- what cheque sizes they genuinely write,

- whether they lead or follow,

- and who inside the fund actually influences decisions.

A lot of founders still approach fundraising like outbound sales activity. Large outreach volumes create the illusion of progress whilst often damaging credibility and momentum underneath because the investment ecosystem is much smaller than many people realise. Investors compare opportunities constantly, speak privately and form views on management teams surprisingly quickly. Poorly targeted outreach, unrealistic valuations, inconsistent information and weak preparation tend to travel far faster than founders expect, particularly within specialist sectors where the same investors repeatedly see the same businesses.

At Kognise, a large part of our role is helping businesses think much more strategically about funding itself before they formally enter the market. That includes understanding:

- the genuine funding requirement,

- which elements are equity versus lending,

- what operational expertise is missing,

- how the business should be structured for scale,

- how IP should be protected,

- and which investors are genuinely aligned with the long-term strategy.

Ultimately the goal should never simply be raising money. The goal should be building a business capable of absorbing capital intelligently, scaling sustainably and remaining investable across multiple future funding cycles rather than constantly reacting to the next short-term funding problem.

-

Why Commercial Pattern Recognition Matters More Than Sector Labels

One of the questions we occasionally get asked at Kognise is why we work across such a broad range of sectors. At the last check, our projects covered everything from entertainment and biosciences through to oil & gas, robotics, retail, food, fashion and energy, across a mixture of start-ups, scale-ups and restructures.

On paper that can sometimes look unusual because many advisory firms position themselves as highly sector-specific. There is absolutely value in deep technical expertise and there are situations where specialist knowledge is critical, particularly in regulated or highly technical industries, but what people often underestimate is how many of the underlying commercial and operational challenges are actually shared across sectors.

The technology changes. The terminology changes. The regulatory environment changes. The underlying business pressures often do not.

Whether we are working with a robotics business trying to industrialise production, a bioscience company preparing for scale, an energy platform expanding internationally or a fashion business restructuring margins and operations, the conversations usually come back to very similar themes:

- capital,

- scalability,

- operational maturity,

- leadership,

- governance,

- market access,

- automation,

- and execution capability.

That is where broad commercial pattern recognition becomes extremely valuable.

At Kognise, one of the first things we try to understand is not simply the business itself, but the people behind it. Every founder and board team arrives with different drivers, ambitions and constraints. Some are trying to scale aggressively into international markets, some are dealing with operational pressure or shareholder complexity, while others have exceptional technology but lack the structure or leadership support needed to unlock commercial growth.

Those starting points matter far more than many people realise because two businesses operating in exactly the same sector can require completely different strategic approaches depending on:

- funding position,

- shareholder dynamics,

- operational maturity,

- leadership capability,

- market timing,

- or international exposure.

This is one of the reasons template-driven advisory often struggles in growth environments. Real businesses rarely scale in neat, predictable ways.

The wider market itself is also changing extremely quickly. PwC estimates AI could contribute as much as $15.7 trillion to the global economy by 2030, whilst McKinsey analysis suggests automation technologies could impact up to 30% of hours worked globally before the end of the decade. At the same time, PitchBook data showed US venture funding exceeding $267bn in Q1 2026 alone, although a disproportionate amount of that capital was concentrated into a relatively small number of AI and infrastructure-related transactions.

That concentration matters because it means businesses outside the most aggressively funded sectors are having to work much harder to demonstrate:

- operational discipline,

- commercial scalability,

- realistic financial control,

- and long-term defensibility.

We are seeing that directly across multiple sectors.

Within entertainment and energy, there is increasing pressure around operational resilience, sustainability and infrastructure modernisation. The global live entertainment market is forecast to exceed $1 trillion over the next decade, but the infrastructure supporting it is simultaneously being pushed towards:

- lower emissions,

- greater energy efficiency,

- improved reporting,

- and more intelligent operational monitoring.

In biosciences, innovation remains exceptionally strong, but investors have become much more selective following the funding surge seen during and immediately after the pandemic years. Scientific innovation alone is no longer enough. Investors increasingly want to understand commercialisation strategy, operational maturity, regulatory realism and how leadership teams intend to scale beyond early-stage research.

Robotics presents another interesting example because market excitement often runs significantly ahead of operational reality. The global robotics market is expected to exceed $200bn within the next several years, driven by labour shortages, AI integration and industrial automation demand. However, scaling robotics businesses remains hugely capital intensive and operationally complex. We regularly see businesses underestimate manufacturing risk, working capital exposure, supply chain fragility and the sheer operational discipline required to move from prototype to scalable deployment.

Retail and fashion are dealing with a different type of pressure altogether. Consumer confidence remains volatile, supply chains are still recovering in places and margin pressure has become a major issue across much of the sector. McKinsey’s State of Fashion reports continue to highlight weaker discretionary spending alongside increasing operational costs and inventory pressure. At the same time, businesses are trying to navigate sustainability expectations, AI-driven consumer behaviour shifts and increasingly global fulfilment complexity.

Meanwhile oil & gas and wider energy markets remain in a period of structural transition. Geopolitical instability and energy security concerns have reinforced the importance of traditional energy infrastructure in the short term, whilst simultaneously accelerating investment into automation, resilience, reporting capability and transition technologies.

One of the interesting things about working across multiple sectors is that ideas and operational approaches increasingly migrate between industries. Automation capability developed in logistics starts becoming relevant in food production. Energy optimisation approaches developed in industrial markets begin moving into entertainment infrastructure. AI-driven monitoring developed for one operational environment quickly becomes useful somewhere entirely different.

That cross-pollination is becoming much more important because the market is no longer rewarding businesses simply for having an interesting idea. Investors are increasingly looking for businesses that can combine:

- innovation,

- operational realism,

- scalability,

- and commercial discipline.

At Kognise, our role is rarely to walk into a business pretending we know more about the client’s specialist market than they do. In most cases the founders and leadership teams understand their sectors exceptionally well. The value comes from helping connect:

- strategy,

- structure,

- funding,

- operational scaling,

- governance,

- automation,

- and execution

in a way that allows the business to move forward more effectively.

That can involve:

- equity and debt funding,

- structuring for growth,

- automation strategy,

- IP positioning,

- legal and international structuring,

- operational scaling,

- access to markets,

- or bringing in highly specialised expertise where needed.

Increasingly it also involves helping businesses navigate uncertainty. The market founders are operating in today is materially more complex than it was even a few years ago. Investors are more cautious, supply chains are more fragile, geopolitical instability is feeding into operational costs and AI is reshaping competitive dynamics across almost every industry.

That environment rewards businesses that are operationally disciplined, strategically adaptable and commercially realistic.

Ultimately, whilst sectors can look very different on the surface, many of the underlying challenges around growth, leadership, scale and execution are remarkably similar. The businesses that tend to perform best over time are usually not the ones with the loudest narrative, but the ones that build the strongest operational foundations underneath it.

-

Fundraising Is Not About Finding Investors. It Is About Building Confidence.

One of the biggest misconceptions founders and scale-up leadership teams have is that fundraising is primarily about the pitch.

They assume the process revolves around:

- a polished deck,

- a compelling story,

- a few investor meetings,

- and enough enthusiasm to convince somebody to write a cheque.

In reality, fundraising is usually a far more demanding exercise in credibility, preparation, operational maturity and risk management.

Investors are not simply assessing whether they like the idea. They are trying to understand whether this business can realistically scale, whether management understands the challenges ahead, and whether the opportunity justifies the level of risk they are about to take on.

That distinction matters because it explains why so many businesses with genuinely good products still fail to raise capital. The problem is rarely just the technology or the market opportunity. More often it is because the business is underprepared, lacks clarity, presents inconsistently, approaches the wrong investors, or simply does not understand how professional funders think and behave.

The statistics themselves are sobering. Research across thousands of startup raises suggests that only a very small percentage of businesses successfully secure institutional funding, particularly at pre-seed and seed stages. At the same time, the number of investor meetings and introductions typically required to close a round has increased significantly over the past few years as markets have tightened and investors have become more selective.

Fundraising has become less about excitement and more about evidence. That evidence sits across:

- the quality of the management team,

- operational maturity,

- financial understanding,

- commercial realism,

- governance,

- market understanding,

- and increasingly, how well a business handles scrutiny under pressure.

This is why experienced investors can often form an opinion about a company surprisingly quickly, sometimes long before the founder has even finished presenting the deck.

Why Pulling Together A Proper Data Room Is So Difficult

Almost every founder underestimates the challenge of building a proper investor-ready data room. From the outside it sounds simple enough:

- upload documents,

- add financials,

- include legal agreements,

- maybe tidy up the cap table,

- and share a link.

In reality, the process is usually far messier. Most growing businesses have evolved quickly and organically. Information is scattered across multiple systems, old forecasts conflict with newer ones, contracts are unsigned or incomplete, assumptions exist inside founders’ heads rather than documented processes, and reporting has often been built reactively rather than strategically.

Once fundraising begins, all of that hidden disorder suddenly becomes visible. The business then finds itself trying to operationalise years of fragmented information whilst simultaneously continuing to run day-to-day operations. That is where many raises begin to lose momentum. Experienced investors immediately notice:

- inconsistencies,

- gaps in governance,

- conflicting numbers,

- unclear ownership,

- weak forecasting assumptions,

- and delayed responses.

None of those things build confidence. Importantly, investors do not view the data room simply as an administrative requirement. They view it as a reflection of how the company itself is run. A well-structured data room demonstrates:

- discipline,

- preparedness,

- operational maturity,

- and leadership control.

A poor one suggests the opposite. That is why businesses often underestimate how much time is required to prepare properly before investor outreach should even begin.

The Pitch Deck And Teaser Deck Serve Completely Different Purposes

Another common issue is businesses trying to force too much into a single deck. The result is usually a document that tries to be:

- a teaser,

- a sales presentation,

- an investor deck,

- a technical overview,

- and an operational business plan

all at the same time. It rarely works. A teaser deck exists to generate interest and secure the next conversation. Its job is not to answer every question. In fact, if it does, it is probably too detailed. The investor deck then expands on:

- the commercial opportunity,

- the problem,

- the solution,

- traction,

- market dynamics,

- scalability,

- financials,

- and the investment proposition itself.

The data room then supports diligence and validation behind those claims. Trying to collapse all three into one usually creates confusion and overwhelms the audience. One of the biggest mistakes founders make is assuming investors want every detail immediately. Most do not. Professional investors review huge volumes of opportunities. They are looking initially for:

- clarity,

- commercial understanding,

- credibility,

- differentiation,

- and evidence that management understands what really matters.

Long, bloated decks filled with excessive technical detail often create the opposite effect. Rather than building confidence, they suggest the business cannot distil its own value proposition clearly. That is particularly dangerous in competitive funding environments where investors are reviewing multiple opportunities simultaneously.

Spray And Pray Fundraising Usually Creates More Damage Than Opportunity

A surprising number of businesses still approach fundraising like outbound sales.

Large mailing lists.

Generic introductions.

Mass deck distribution.

Hundreds of cold approaches.It creates activity, but not necessarily progress. Professional investors are highly specialised. Most funds operate within defined parameters around:

- sector focus,

- stage,

- geography,

- cheque size,

- risk appetite,

- and portfolio strategy.

Approaching investors who fundamentally do not align with the business wastes enormous amounts of time and often damages momentum internally. Worse still, poorly targeted outreach can create reputational issues within investor networks, particularly when founders appear unprepared or unclear about why they are approaching specific funds. The strongest fundraising processes are normally highly curated. Good founders spend time understanding:

- who genuinely invests in their sector,

- who understands the market,

- who can support future rounds,

- who has relevant operational experience,

- and who is likely to align culturally with the leadership team.

Not all capital is equal. Some investors bring strategic value, operational guidance, networks and long-term support. Others can create friction, misalignment and short-term pressure that damages the business over time. Choosing investors should therefore be viewed as a long-term strategic decision rather than simply solving an immediate funding problem.

Investors Are Assessing The Team Far More Than Most Founders Realise

Founders often believe investors are primarily investing into:

- the product,

- the technology,

- or the market opportunity.

In reality, particularly at early and growth stages, investors are usually investing into the management team’s ability to navigate uncertainty. Because every business encounters problems.

Markets shift.

Forecasts change.

Competitors emerge.

Hiring becomes difficult.

Margins tighten.

Technology evolves.Experienced investors know all of that already. What they are trying to determine is whether the leadership team:

- understands the business deeply,

- communicates clearly,

- operates with discipline,

- makes rational decisions,

- and can scale without losing control operationally.

That is why practising and refining the pitch matters so much. The best pitches rarely feel over-rehearsed or robotic. They feel confident, commercially grounded and natural because the management team has already pressure-tested:

- the narrative,

- the assumptions,

- the objections,

- and the difficult questions.

Repetition exposes weaknesses before investors do. It also helps leadership teams simplify complexity, which is an underrated but hugely important skill during fundraising.

Having The Right People In The Room Changes Investor Confidence

One of the clearest signals investors look for is whether there is genuine depth within the management team. Businesses sometimes send only the founder into fundraising meetings, particularly in earlier stages. While that can work in some circumstances, scale-up investors in particular usually want to see broader operational capability. They are assessing whether the company can realistically scale delivery, operations and governance alongside growth.

That is why having the right mix of people involved matters. Strong investor discussions often include representation across:

- strategy,

- commercial leadership,

- marketing,

- operations,

- delivery,

- and finance.

Not because every person needs to dominate the conversation, but because investors observe how leadership teams function together. They notice:

- whether responsibilities are clear,

- whether numbers are understood consistently,

- whether operational realities are appreciated,

- and whether the leadership team behaves like an organisation capable of scaling.

The dynamics in the room often tell investors more than the deck itself.

Understanding The Investor’s World Helps Founders Navigate The Process Better

One of the most useful mindset shifts for founders is recognising that investors themselves operate under significant pressure. Funds answer to:

- investment committees,

- LPs,

- portfolio expectations,

- deployment targets,

- reserve strategies,

- and return requirements.

The current market environment has also changed investor behaviour materially. Whilst sectors such as AI continue attracting large amounts of capital, many funds themselves are facing fundraising pressure, slower exits and increased scrutiny around portfolio performance. That changes how investors behave.

Processes become slower.

Diligence becomes deeper.

Decision-making becomes more cautious.

Internal consensus becomes more important.From a founder’s perspective this can feel frustrating, particularly when investor engagement appears positive but timelines continue extending. Often this is not lack of interest. It is the reality of how investment firms themselves operate internally. The best founders understand this and adapt accordingly. Rather than trying to aggressively “sell” to investors, they focus on progressively building conviction through:

- clarity,

- responsiveness,

- consistency,

- preparation,

- and operational credibility.

There is a major difference between creating excitement and creating confidence. Professional investors ultimately invest when they believe risk is being understood and managed intelligently.

Why Experienced Advisors Create So Much Value

Many founders assume advisors are primarily useful because they can make introductions. Good advisors do far more than that. An experienced advisor helps businesses:

- structure the process,

- improve positioning,

- refine messaging,

- identify weaknesses,

- prepare for diligence,

- challenge unrealistic assumptions,

- and maintain momentum through what is often an exhausting process.

Importantly, experienced advisors also bring perspective. Because fundraising can distort judgement internally. Founders become emotionally attached to narratives, assumptions and forecasts that may not stand up to external scrutiny. A good advisor helps bridge the gap between:

- how founders see the business,

- and how investors are likely to evaluate it.

That difference is often where successful raises are won or lost. The strongest fundraising processes are rarely accidental. They are normally the result of disciplined preparation, clear communication, operational maturity and continuous refinement. And increasingly, in tighter funding markets, those qualities matter more than ever.

-

I attended the inaugural Cheshire and Warrington Combined Authority board meeting this week.

I attended the inaugural Cheshire and Warrington Combined Authority board meeting this week. There’s a lot of energy in the room. But more importantly, there’s a clear recognition that this is not about creating another layer of structure. It’s about whether we can actually shift outcomes.

The Get Cheshire & Warrington Working Plan sets the context well. On paper, this is one of the strongest economies in the North. High employment, strong sectors, good earnings. But scratch the surface and the gaps are obvious. We still have over 100,000 people economically inactive. Long-term sickness is rising. Early retirement is a major factor. And there are 65,000+ people on Universal Credit who have been out of work for over a year.

At the same time, employers are struggling to recruit. That disconnect is the real issue. Not a lack of opportunity, but a failure to connect people to it in a way that actually works.

What stood out

The plan is honest about where the problems sit.

It identifies six priority groups, which broadly come down to:

- people disconnected from opportunity

- people held back by health

- people falling through transition points

- and people in places where access simply doesn’t work

This is not new insight. But the difference here is the intent to treat it as a system problem, not a programme problem. That matters, because the current landscape is fragmented. DWP, NHS, local authorities, skills providers, employers, voluntary sector… all doing something, but rarely aligned. The plan calls that out directly and pushes toward a joined-up, locally driven employment system rather than a collection of initiatives.

The real test

The next 12–18 months are critical.

The plan talks about:

- governance to align delivery

- auditing existing provision (and stripping duplication)

- targeted task groups for priority issues

- and moving toward a single strategic employment support model

These are all sensible but this only works if it goes beyond coordination and into control and accountability. Devolution gives Cheshire & Warrington a real opportunity here. Not just to shape policy, but to redesign how the system actually operates on the ground.

That includes:

- how funding flows

- how outcomes are measured

- and how employers are genuinely brought into the solution

The bit that needs more focus

If there is a gap, it’s this, we still risk over-indexing on supporting people into work without equally addressing how employers behave. The plan touches on this, particularly around:

- low investment in workforce training

- lack of progression pathways

- and limited incentives to take on early talent

But this needs to be more central, because without changing employer behaviour, we’re just recycling people through the same system.

Final thought

There is no shortage of strategy in this space. What’s different here is the platform:

- devolution

- aligned partners

- and a clear economic case to act

If this turns into a genuinely integrated system, it will move the dial. If it becomes another well-written plan with loosely connected delivery, it won’t. Simple as that.

-

The Case For Sustainability Practices

An advisory perspective from Kognise & Responsible Business ESG

Sustainability is no longer a positioning choice; it is becoming a structural requirement that influences how businesses access capital, secure contracts and manage cost.

This shift is now visible in how decisions are made. Sustainability criteria are embedded into procurement processes across large corporates, while investors increasingly expect structured ESG data alongside financials. At the same time, frameworks such as CSRD are moving sustainability disclosure closer to financial reporting standards. The combined effect is that sustainability is no longer assessed qualitatively; it is being evaluated as part of commercial and investment decision-making.

The implication is straightforward. Businesses are being assessed on whether sustainability is embedded into their operating model, not whether it is described in their narrative. Those that can evidence it are progressing. Those that cannot are increasingly filtered out early.

Where Kognise & Responsible Business ESG operate

Most businesses do not lack intent. The issue is translation, turning sustainability from concept into something that is structured, measurable and commercially relevant.

Kognise works with founders, boards and investors at points where capital, strategy and execution need to align. Responsible Business ESG brings the capability to translate sustainability into operational programmes, reporting structures and governance that stand up to scrutiny. Together, the focus is on ensuring sustainability is not positioned alongside the business, but integrated into it in a way that supports funding, procurement and delivery.

In practice, this means establishing a clear baseline, structuring data and governance, linking sustainability to cost, revenue and risk, embedding it into the operating model, and ensuring consistency across all materials and interactions. The outcome is not a narrative. It is something that can be evidenced and relied upon.

From narrative to evidence

Sustainability is now assessed on structure, consistency and evidence rather than intent. That requires comparable and defensible data, repeatable methodologies and claims that can be explained under scrutiny. Governance also becomes visible, with clear ownership and accountability expected at leadership level.

CSRD reinforces this direction by formalising expectations around disclosure and materiality. Its impact extends beyond those directly in scope, as businesses are increasingly required to provide structured sustainability data through supply chains and investor processes. Even where reporting is not mandatory, scrutiny is increasing and expectations are converging.

Sustainability as a commercial driver

Sustainability is influencing core commercial mechanics rather than sitting alongside them. Energy, materials and logistics are no longer stable inputs, and businesses that reduce exposure through efficiency or system redesign improve cost predictability and resilience. Procurement is evolving in parallel, with sustainability embedded into buying decisions, particularly within large corporates and institutional supply chains. This creates a direct link between sustainability and revenue access.

Risk is tightening at the same time, with regulatory pressure, supply chain expectations and operational exposure converging. Sustainability provides a structured way to manage these pressures, but only when it is embedded into operations. The result is that sustainability is becoming part of the commercial model rather than a discretionary layer.

Where this is already visible

This shift is evident across multiple parts of the value chain, although it presents differently depending on where the leverage sits.

Showpower — Energy as infrastructure

Showpower supporting Coldplay at Wembley In live events and temporary power environments, diesel generation has historically been the default, despite its cost volatility and operational inefficiency. Showpower’s model reframes this by treating energy as infrastructure. Battery integration, combined with renewable inputs where available, reduces reliance on diesel while improving delivery certainty and operational control.

This has a direct commercial impact. Diesel can account for a significant proportion of temporary power costs on large-scale events, and exposure to fuel price volatility introduces both cost risk and planning uncertainty. By displacing diesel usage, Showpower reduces that exposure while improving predictability across deployments.

From an environmental perspective, temporary power is often a material contributor to event emissions. In parallel, broader event emissions profiles are heavily weighted toward logistics and travel, which can represent over 60% of total emissions in large touring environments. This concentration increases scrutiny on energy systems, as they remain one of the most visible and controllable components.

The result is a model where sustainability is not the objective in isolation. It is a function of improving cost control, resilience and delivery capability.

Measurable Energy Smart Technology measurable.energy addresses a different part of the problem, focusing on wasted electricity within buildings, particularly plug-load energy that is typically unmanaged but material at scale.

Its model combines proprietary hardware with a high-margin SaaS layer to monitor and control energy usage at appliance level. This creates a direct and measurable link between energy reduction and cost saving. Across its existing customer base, the platform has demonstrated reductions in plug-load energy consumption that translate into immediate operational savings, with reported SaaS margins in excess of 90% and net revenue retention above 100%.

At a deployment level, even relatively small estates can remove several tonnes of CO₂ annually while delivering payback through reduced energy spend. The commercial logic is clear. Sustainability is not being introduced as an additional cost; it is improving efficiency and margin.

Hope Solutions operates as the translation layer, turning sustainability ambition into structured, measurable programmes across carbon, procurement and supply chains.

Its role is to make sustainability executable and aligned with both regulatory requirements and commercial expectations, particularly in complex environments such as live events and media.Loom reflects a shift on the demand side, extending the usable life of clothing and reducing reliance on new production. This reduces embedded emissions and material throughput while reshaping consumption economics. Across these examples, the pattern is consistent. Sustainability is shaping how businesses operate, not how they describe themselves.

The gap most businesses face

The issue is rarely awareness. It is translation. Sustainability is often overstated without supporting data, disconnected from financial performance, or inconsistently presented across materials and operations. In many cases, it remains a communications layer rather than an operating discipline.

These gaps are increasingly visible. Investors and corporates are applying structured screening processes to assess alignment between narrative and evidence. Where inconsistencies appear, confidence drops quickly and opportunities are lost early.

What CSRD is changing in practice

CSRD is not simply a reporting requirement; it is driving structural change in how sustainability is understood and applied.

Double materiality links sustainability directly to financial performance, requiring businesses to assess both their impact and their exposure. Scope 3 emissions bring supply chains into focus, particularly in sectors where the majority of emissions sit outside direct control. Governance expectations shift responsibility into leadership, with clear accountability for reporting and decision-making. This is where many businesses remain underdeveloped.

Investor lens

Sustainability assessment is becoming more consistent. Businesses that progress demonstrate a clear linkage between sustainability and commercial performance, supported by data and embedded into operations. Consistency across materials and governance is expected.

Those that struggle present sustainability in isolation, without clear connection to cost, revenue or risk. High-level claims without supporting data, or inconsistencies between narrative and execution, are often enough to prevent further engagement. This filtering is increasingly front-loaded.

How sustainability should be communicated

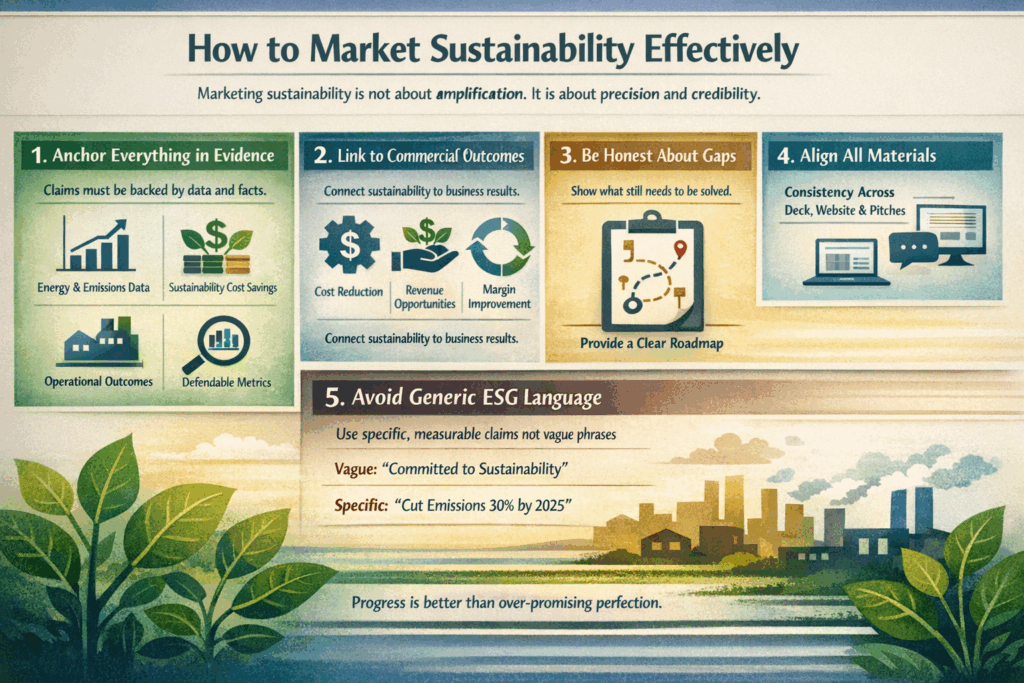

Most issues seen in investor and procurement processes are not driven by lack of activity, but by how that activity is presented. Sustainability is often overstated or disconnected from the commercial model. In both cases, it reduces credibility. The objective is not amplification. It is precision.

Claims need to be supported by data that can be explained and defended, including energy usage, emissions impact, cost outcomes and operational change. Sustainability should be clearly linked to commercial drivers such as cost reduction, revenue access and risk management. Credibility increases when businesses are explicit about what remains unresolved and present a defined roadmap rather than an over-claimed position.

Consistency across deck, data room, website and commercial discussions is critical, as misalignment is identified quickly and interpreted as a lack of control. Generic ESG language adds little value without context or metrics; specificity and evidence are what differentiate credible businesses.

Take-away

Sustainability is no longer a parallel agenda or a communications layer. It is a commercial and structural requirement that influences how businesses operate, compete and access capital. Businesses that embed it into their operating model are already seeing advantages in cost, access to revenue and capital. Those that continue to position it separately are encountering friction early, often before meaningful engagement takes place.

The direction is clear. Sustainability is now assessed on evidence, consistency and performance. The question is no longer whether to act, but whether the business is structured to withstand scrutiny when it does.

Anthony King, Kognise

“Sustainability is increasingly a proxy for how well a business is built. Cost, risk and capital all converge here. If it isn’t embedded in the operating model, it won’t stand up to scrutiny.” -

Investment Readiness and Capital Strategy Structure, Process and Execution

1. Objective

This guide sets out how investment actually works in practice, not as a theoretical exercise but as a structured process that founders and investors move through together. The aim is to clarify how capital is assessed, how decisions are made, and how businesses should position themselves to raise effectively and deploy capital well once secured.

At its core, this is about aligning three things: the needs of the business, the expectations of investors, and the realities of execution.

2. What Investment Really Is

Investment is often misunderstood as a transaction. In reality, it is an exchange of risk for future value, where capital is provided today in return for a share of an uncertain outcome tomorrow.

From an investor’s perspective, the business in its current form is only part of the equation. What matters is whether that business can convert capital into scalable, defensible value over time. This is why two businesses with similar products can receive very different outcomes in a raise. One demonstrates a credible pathway to scale, the other does not.

For founders, this means the focus should not be on securing capital as an endpoint, but on building a business that justifies investment in the first place.

3. The Investment Lifecycle

Raising capital is not a single event. It is a sequence of stages, each of which builds on the last and each of which introduces its own failure points.

The process begins with preparation. At this stage, the business must be able to clearly articulate what it does, who it serves, and how it generates value. This is supported by a coherent financial model and a narrative that links strategy to execution. Most failed raises can be traced back to weaknesses here, where the story and the numbers do not align.