The Case For Sustainability Practices

An advisory perspective from Kognise & Responsible Business ESG

Sustainability is no longer a positioning choice; it is becoming a structural requirement that influences how businesses access capital, secure contracts and manage cost.

This shift is now visible in how decisions are made. Sustainability criteria are embedded into procurement processes across large corporates, while investors increasingly expect structured ESG data alongside financials. At the same time, frameworks such as CSRD are moving sustainability disclosure closer to financial reporting standards. The combined effect is that sustainability is no longer assessed qualitatively; it is being evaluated as part of commercial and investment decision-making.

The implication is straightforward. Businesses are being assessed on whether sustainability is embedded into their operating model, not whether it is described in their narrative. Those that can evidence it are progressing. Those that cannot are increasingly filtered out early.

Where Kognise & Responsible Business ESG operate

Most businesses do not lack intent. The issue is translation, turning sustainability from concept into something that is structured, measurable and commercially relevant.

Kognise works with founders, boards and investors at points where capital, strategy and execution need to align. Responsible Business ESG brings the capability to translate sustainability into operational programmes, reporting structures and governance that stand up to scrutiny. Together, the focus is on ensuring sustainability is not positioned alongside the business, but integrated into it in a way that supports funding, procurement and delivery.

In practice, this means establishing a clear baseline, structuring data and governance, linking sustainability to cost, revenue and risk, embedding it into the operating model, and ensuring consistency across all materials and interactions. The outcome is not a narrative. It is something that can be evidenced and relied upon.

From narrative to evidence

Sustainability is now assessed on structure, consistency and evidence rather than intent. That requires comparable and defensible data, repeatable methodologies and claims that can be explained under scrutiny. Governance also becomes visible, with clear ownership and accountability expected at leadership level.

CSRD reinforces this direction by formalising expectations around disclosure and materiality. Its impact extends beyond those directly in scope, as businesses are increasingly required to provide structured sustainability data through supply chains and investor processes. Even where reporting is not mandatory, scrutiny is increasing and expectations are converging.

Sustainability as a commercial driver

Sustainability is influencing core commercial mechanics rather than sitting alongside them. Energy, materials and logistics are no longer stable inputs, and businesses that reduce exposure through efficiency or system redesign improve cost predictability and resilience. Procurement is evolving in parallel, with sustainability embedded into buying decisions, particularly within large corporates and institutional supply chains. This creates a direct link between sustainability and revenue access.

Risk is tightening at the same time, with regulatory pressure, supply chain expectations and operational exposure converging. Sustainability provides a structured way to manage these pressures, but only when it is embedded into operations. The result is that sustainability is becoming part of the commercial model rather than a discretionary layer.

Where this is already visible

This shift is evident across multiple parts of the value chain, although it presents differently depending on where the leverage sits.

Showpower — Energy as infrastructure

In live events and temporary power environments, diesel generation has historically been the default, despite its cost volatility and operational inefficiency. Showpower’s model reframes this by treating energy as infrastructure. Battery integration, combined with renewable inputs where available, reduces reliance on diesel while improving delivery certainty and operational control.

This has a direct commercial impact. Diesel can account for a significant proportion of temporary power costs on large-scale events, and exposure to fuel price volatility introduces both cost risk and planning uncertainty. By displacing diesel usage, Showpower reduces that exposure while improving predictability across deployments.

From an environmental perspective, temporary power is often a material contributor to event emissions. In parallel, broader event emissions profiles are heavily weighted toward logistics and travel, which can represent over 60% of total emissions in large touring environments. This concentration increases scrutiny on energy systems, as they remain one of the most visible and controllable components.

The result is a model where sustainability is not the objective in isolation. It is a function of improving cost control, resilience and delivery capability.

measurable.energy addresses a different part of the problem, focusing on wasted electricity within buildings, particularly plug-load energy that is typically unmanaged but material at scale.

Its model combines proprietary hardware with a high-margin SaaS layer to monitor and control energy usage at appliance level. This creates a direct and measurable link between energy reduction and cost saving. Across its existing customer base, the platform has demonstrated reductions in plug-load energy consumption that translate into immediate operational savings, with reported SaaS margins in excess of 90% and net revenue retention above 100%.

At a deployment level, even relatively small estates can remove several tonnes of CO₂ annually while delivering payback through reduced energy spend. The commercial logic is clear. Sustainability is not being introduced as an additional cost; it is improving efficiency and margin.

Hope Solutions operates as the translation layer, turning sustainability ambition into structured, measurable programmes across carbon, procurement and supply chains.

Its role is to make sustainability executable and aligned with both regulatory requirements and commercial expectations, particularly in complex environments such as live events and media.

Loom reflects a shift on the demand side, extending the usable life of clothing and reducing reliance on new production. This reduces embedded emissions and material throughput while reshaping consumption economics. Across these examples, the pattern is consistent. Sustainability is shaping how businesses operate, not how they describe themselves.

The gap most businesses face

The issue is rarely awareness. It is translation. Sustainability is often overstated without supporting data, disconnected from financial performance, or inconsistently presented across materials and operations. In many cases, it remains a communications layer rather than an operating discipline.

These gaps are increasingly visible. Investors and corporates are applying structured screening processes to assess alignment between narrative and evidence. Where inconsistencies appear, confidence drops quickly and opportunities are lost early.

What CSRD is changing in practice

CSRD is not simply a reporting requirement; it is driving structural change in how sustainability is understood and applied.

Double materiality links sustainability directly to financial performance, requiring businesses to assess both their impact and their exposure. Scope 3 emissions bring supply chains into focus, particularly in sectors where the majority of emissions sit outside direct control. Governance expectations shift responsibility into leadership, with clear accountability for reporting and decision-making. This is where many businesses remain underdeveloped.

Investor lens

Sustainability assessment is becoming more consistent. Businesses that progress demonstrate a clear linkage between sustainability and commercial performance, supported by data and embedded into operations. Consistency across materials and governance is expected.

Those that struggle present sustainability in isolation, without clear connection to cost, revenue or risk. High-level claims without supporting data, or inconsistencies between narrative and execution, are often enough to prevent further engagement. This filtering is increasingly front-loaded.

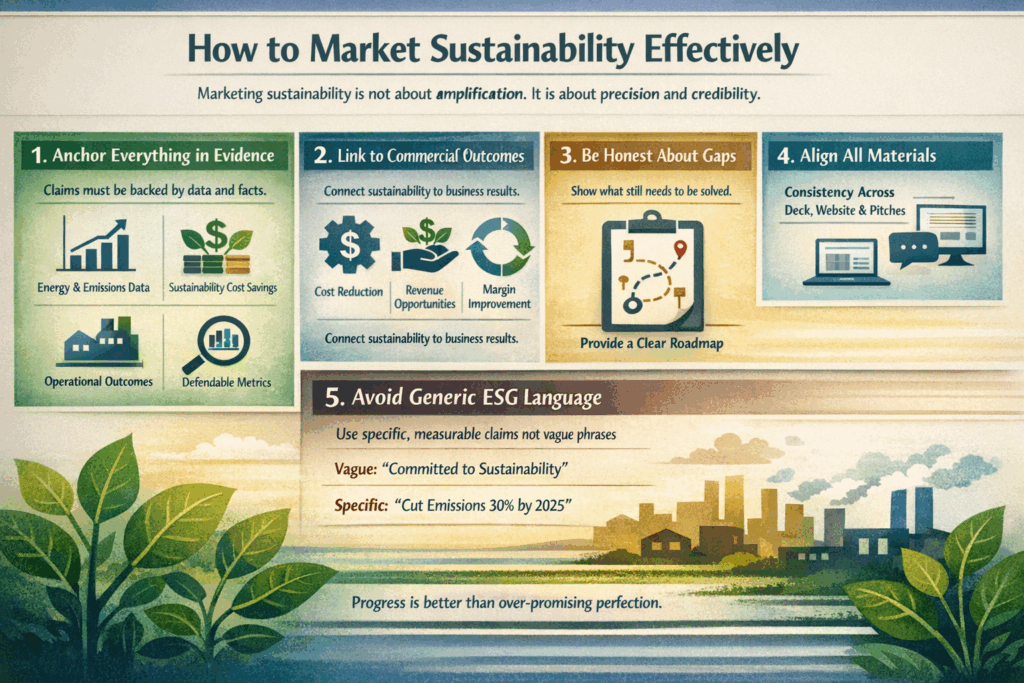

How sustainability should be communicated

Most issues seen in investor and procurement processes are not driven by lack of activity, but by how that activity is presented. Sustainability is often overstated or disconnected from the commercial model. In both cases, it reduces credibility. The objective is not amplification. It is precision.

Claims need to be supported by data that can be explained and defended, including energy usage, emissions impact, cost outcomes and operational change. Sustainability should be clearly linked to commercial drivers such as cost reduction, revenue access and risk management. Credibility increases when businesses are explicit about what remains unresolved and present a defined roadmap rather than an over-claimed position.

Consistency across deck, data room, website and commercial discussions is critical, as misalignment is identified quickly and interpreted as a lack of control. Generic ESG language adds little value without context or metrics; specificity and evidence are what differentiate credible businesses.

Take-away

Sustainability is no longer a parallel agenda or a communications layer. It is a commercial and structural requirement that influences how businesses operate, compete and access capital. Businesses that embed it into their operating model are already seeing advantages in cost, access to revenue and capital. Those that continue to position it separately are encountering friction early, often before meaningful engagement takes place.

The direction is clear. Sustainability is now assessed on evidence, consistency and performance. The question is no longer whether to act, but whether the business is structured to withstand scrutiny when it does.

Anthony King, Kognise

“Sustainability is increasingly a proxy for how well a business is built. Cost, risk and capital all converge here. If it isn’t embedded in the operating model, it won’t stand up to scrutiny.”