-

SCI-TECH DARESBURY BUSINESS BREAKFAST NETWORKING EVENT – April 19th

We will be attending the Sci-Tech Daresbury Business Breakfast networking event on April 19th. NetworkHub is Sci-Tech Daresbury’s virtual network of around 5,000 people across the North West of England and beyond. NetworkHub brings together all of the expertise needed to accelerate the development and growth of technology companies.

NetworkHub runs 10 of these each year on a Friday morning from 8am to 9.30am with typically 100 to 150 people attending.

-

Looking Ahead: A Promising Outlook for UK Ventures in 2024

After navigating through the turbulence of recent years, 2023 emerged as a beacon of stability, with investment levels bouncing back to pre-COVID norms. Yet, despite this resurgence, challenges loomed large, with VC funding witnessing a significant dip and investors exercising caution amidst market uncertainties.

So, what does the horizon hold for 2024?

While some forecasts paint a cautious picture, there are glimmers of optimism on the horizon. The British Venture Capital Association (BVCA) hints at a cautious yet hopeful sentiment, urging founders and companies to weather the storm in anticipation of brighter days ahead.

With investors armed with capital reserves from the previous year, there’s a palpable eagerness to seize opportunities in the market. Heavyweights like Mercia Asset Management are gearing up to ramp up investment activities, signaling renewed confidence in the startup landscape.

Furthermore, initiatives like channeling pension funds into startups promise to inject fresh vitality into the ecosystem, although their impact may take time to materialize fully.

However, external factors, including geopolitical tensions and economic scars from the pandemic, cast a shadow of uncertainty. Yet, amidst these challenges, sectors like AI, CleanTech, and HealthTech remain resilient, drawing sustained investor interest.

ESG criteria are increasingly influencing investment decisions, with a growing emphasis on sustainability and decarbonization. The call for green growth echoes loudly, presenting a ripe opportunity for businesses to align with environmental objectives and secure investments.

Despite the cautious optimism, 2024 won’t be without its hurdles. Securing funding, valuations, and strategic backers will demand meticulous planning and perseverance. Founders and management teams must exercise prudence, ensuring robust financial projections and realistic goals.

As the VC market navigates uncertainties, the M&A landscape emerges as an alternative avenue for growth. Tech, Pharma, and Energy giants are on the lookout for strategic acquisitions, presenting scaling businesses with opportunities for partnerships and exits.

In navigating the road ahead, scaling businesses are advised to:

- Ensure meticulous documentation, maintaining organized data rooms for seamless sharing.

- Plan meticulously, setting realistic timelines and anticipating prolonged decision-making processes.

- Seek out experienced advisors early on, forging partnerships with legal and financial experts well-versed in scaling businesses’ needs.

While the journey ahead may be dotted with challenges, it’s the resilience, foresight, and strategic planning of founders and management teams that will steer UK ventures towards a brighter future in 2024 and beyond.

-

Embracing Bright Horizons: Exciting Trends Shaping the Future of the UK

Amidst the twists and turns of a post-pandemic world, UK’s vibrant startup scene is thriving despite economic headwinds and global uncertainties. While 2023 witnessed a dip in VC investments, innovative businesses are charging ahead with optimism and resilience, undeterred by challenges.

Beneath the surface, there’s a silver lining. Despite market fluctuations, funding avenues remain open for ambitious scaleup ventures. Investors are now seeking out innovative ventures with solid foundations and sustainable growth models, signaling a shift towards prudent investment strategies.

The UK government is doubling down on its support for entrepreneurship and innovation. With innovation at the forefront of economic recovery plans, significant investments are pouring into initiatives aimed at nurturing startups and fostering growth.

Looking ahead to 2024, the UK startup landscape is set to dazzle with exciting trends:

- Paving the Way to a Greener Future: Sustainability is taking center stage, driven by a collective commitment to combat climate change. Startups in eco-conscious sectors like Healthtech and Greentech are leading the charge, offering innovative solutions to environmental challenges.

- The Sharing Economy Revolution: In a world where sharing is caring, startups are pioneering platforms that promote resource-sharing and community collaboration. As awareness of environmental issues grows, the sharing economy is gaining momentum, offering sustainable alternatives to traditional consumption patterns.

- The AI Renaissance: Artificial Intelligence (AI) continues to reign supreme, transforming industries with its endless possibilities. From revolutionizing data analytics to powering autonomous systems, AI is reshaping the way we live and work, fueling a wave of innovation across sectors.

As the UK startup ecosystem embraces these trends, a spirit of optimism and innovation permeates the air. Despite the hurdles, the future looks bright as entrepreneurs and investors alike come together to shape a tomorrow filled with endless possibilities and boundless opportunities.

-

UK Tech Start-up Ecosystem Thrives Despite Funding Downturn

Amidst global economic shifts, the United Kingdom stands firm as a formidable player in the tech start-up arena, boasting the world’s sixth-largest economy and securing the third position in funding received during the first quarter of 2024, trailing only behind the US and China.

As of March 15, 2024, the UK’s tech start-up ecosystem has garnered a total of £2.5 billion in funding, marking a 19% decrease from the previous quarter and an 18% decline compared to the same period in 2023.

The decline in funding has been particularly felt in late-stage investments, witnessing a notable 33% reduction from the previous quarter. However, there is a glimmer of hope as early-stage funding only saw a 7% drop, while seed-stage investments experienced a promising 12% increase, signifying ongoing support for budding start-ups.

Despite the overall downturn, notable companies like Monzo, Flagstone, Mews, and Build a Rocket Boy managed to secure substantial funding rounds. Mews, in particular, emerged as the quarter’s standout, becoming the sole new Unicorn following a successful Series D round.

In terms of sectors, FinTech, Enterprise Applications, and Life Sciences emerged as frontrunners, with FinTech leading the pack with a staggering £1 billion in funding. The Enterprise Applications sector witnessed an impressive 90% surge in funding, highlighting growing investor interest in this domain.

London continues to be the epicenter of funding activities, with start-ups in the capital raising a whopping £1.7 billion. However, cities like Edinburgh and Cambridge have also made notable contributions to the funding landscape.

Key investors such as Techstars, Mercia, and Scottish Enterprise play a crucial role in fueling the growth of the UK tech sector. Episode 1 Ventures, Hoxton Ventures, and Northstar Ventures lead the charge in seed-stage investments, while Notion, Octopus Ventures, and Taiwania Capital stand out as prominent early-stage investors. Late-stage investment rounds are spearheaded by CapitalG, Sprints, and Alignment Growth.

Despite challenges, including funding downturns, the UK remains resilient and continues to attract investment. The government’s commitment to fostering growth and innovation in the tech sector is evident through initiatives such as a £1.5 million investment in a marketing campaign.

As the journey unfolds, the UK’s tech start-up ecosystem remains a vibrant and dynamic force on the global stage, poised for further growth and success.

-

2024 is a big year for the UK

As the dawn of the new year breaks, Britain finds itself amidst both real and economic turmoil. However, amidst the concerns lie glimmers of optimism regarding economic and market prospects.

Firstly, as the pandemic crisis wanes into memory, the inflation crisis that ensued is gradually receding into the background.

Secondly, despite dire predictions, the UK economy managed to sidestep a severe recession last year. While it may have skirted close to a mild recession, the exact status remains uncertain until the Office for National Statistics (ONS) releases data for the last quarter.

Thirdly, with inflation easing, household financial pressures are alleviating. Real wage growth is restoring purchasing power, likely driving an uptick in retail spending. Many households have also rebuilt their savings buffers lost during the previous year.

The stabilizing macroeconomic environment is fostering business confidence and encouraging investment for the future, as indicated by positive signs in recent business surveys.

Lower mortgage rates are expected to spur deals, benefiting the estimated 1.5 million households needing to remortgage this year.

The Centre for Economics and Business Research (CEBR) forecasts that the UK will maintain its position as the world’s sixth-largest economy and grow faster than France in the coming years. Additionally, India is projected to become the world’s third-largest economy by 2035.

Potential tax cuts in the upcoming Budget on March 6 and anticipated interest rate adjustments both in the UK and the US are likely to buoy the stock market. Despite the Bank of England’s cautious stance due to strong wage growth, the outlook for returns remains promising, especially given the value of domestic listed companies.

However, significant challenges persist, including the lagged effects of high interest rates on the economy and employment, the nation’s high tax burden, and historical low levels of investment, hindering growth.

Most economists predict modest growth for the year ahead, ranging from 0 to 0.7 percent. The Resolution Foundation highlights the need for a new economic strategy to reverse decades of underinvestment and capitalize on Britain’s strengths.

Suggestions include supporting high-value-added manufacturing firms, signing new service trade agreements, harnessing education for growth, and boosting productivity in second-tier cities.

Additionally, there is concern about the increasing foreign ownership of British companies, which could lead to short-term profit focus at the expense of long-term investment.

Calls for significant policy reforms, a new growth strategy, and increased government spending on research and development are growing louder. With a newly formed government possessing a fresh mandate, there is potential for real change. As the challenges of the pandemic and inflation ease and climate change becomes more pressing, now may be the opportune moment for transformative action.

-

Easter Spring Footprints Family Office Cocktail Evening

We had an amazing time at the Easter Spring Footprints Family Office cocktail evening at the Washington Hotel in Mayfair! The presentations were incredible and the networking opportunities were top-notch. Huge thanks to Karen Melonie Gould and her team for hosting such a brilliant event. Grateful for the kind invitation.

-

UK Tech in 2024

The below includes some of the key takeaways from our recent report on the state of UK tech heading into 2024, the current health of the ecosystem through a venture capital, geographic and sectoral lens, with HSBC Innovation Banking.

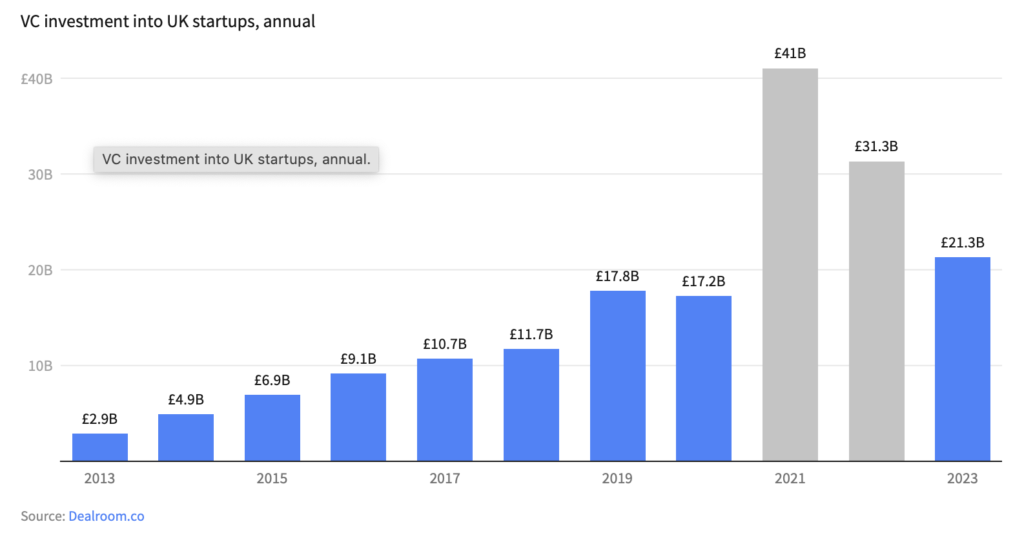

Venture capital in the UK reached an all-time high in 2023 (if you exclude the outlier years of 2021 & 2022).

UK start-ups raised $21.3B in 2023, the third highest total on record, after just the outlier years of 2021/22.

- VC investment has been growing again as of H2 2023.

- Investment up 46% in the second half of 2023, compared to the period Jan-Jun.

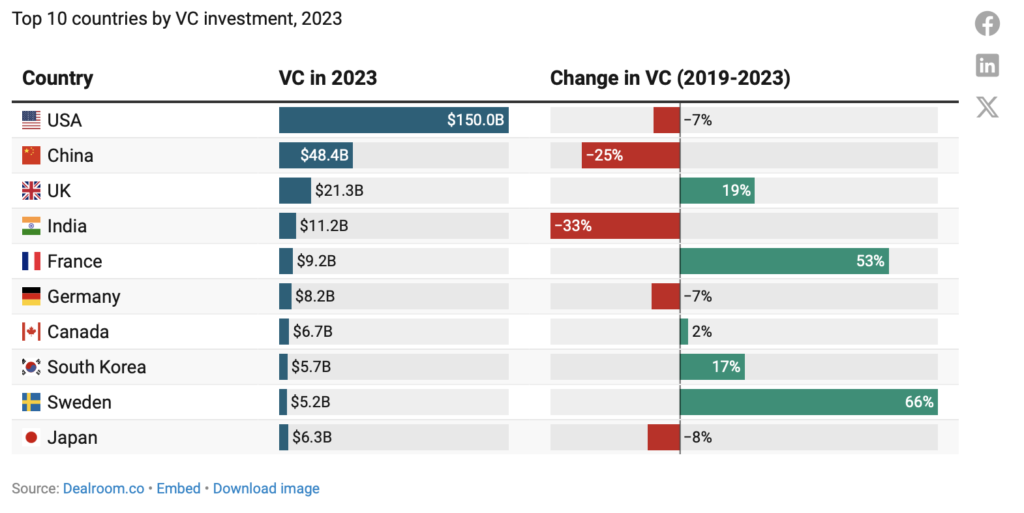

- UK remains the #3 tech ecosystem in the world, 1st in Europe.

UK remains the #3 tech ecosystem in the world, only behind the US and China.

However, on the European scene, UK start-ups raised more than 2nd and 3rd placed France and German start-ups combined.

AI and Climate tech are the UK hottest startup segments.

- Benchmark the UK ecosystem by VC investment, unicorns, new funds as well as other metrics against its European and Global counterparts here on the platform.

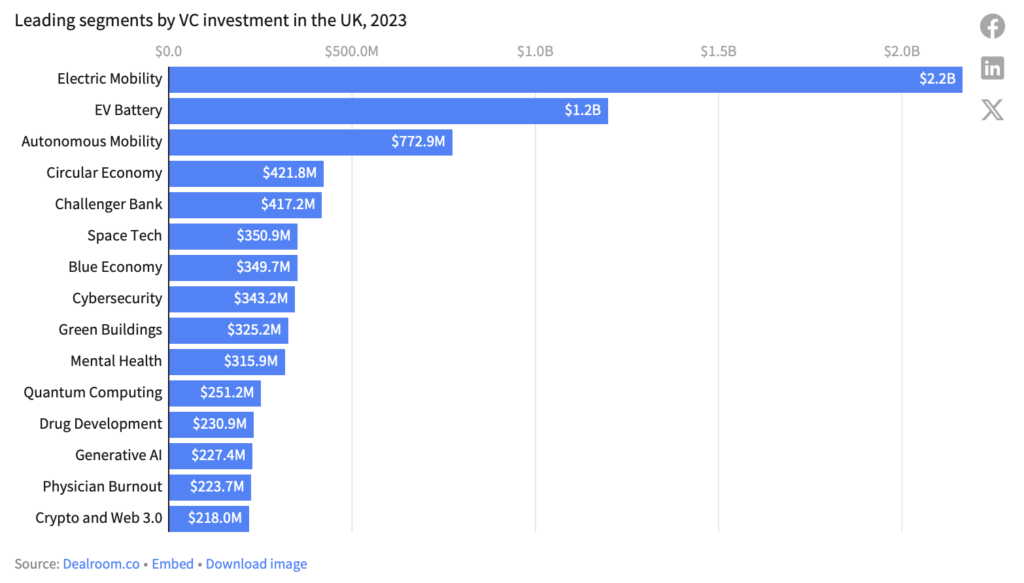

- Electric mobility, EV battery tech and Autonomous mobility were the top funded UK start-up segments in 2023.

- Climate tech accounted for 29% of all UK VC investment in 2023 – $6.2B, an all-time high. This represented 40% growth year on year.

- Start-ups utilising AI raised $4.5B in investment in 2023, including significant rounds for Generative AI companies Synthesia ($90M), AutogenAI ($22.3M & $39.5M) and Stability AI ($50M).

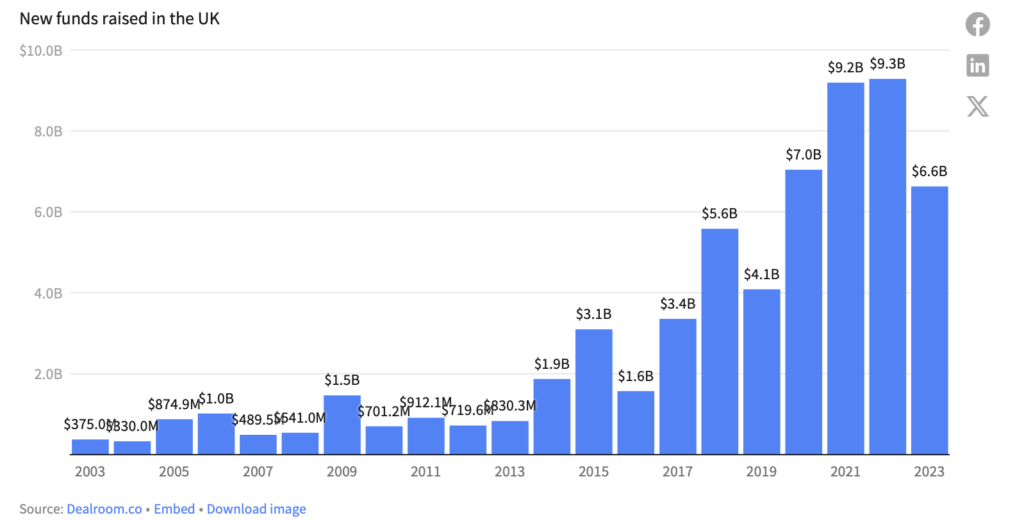

UK investors are armed with over $25B new funds raised in the last 3 years

Over $25B raised in the last three years in the UK.

Leading UK funds are freshly equipped to deploy in 2024.

The UK is the home of European venture capital with 40% of new European VC capital raised in the last five years being based in the UK.